Refinance Mortgage Gilroy: The 2026 Homeowner’s Guide to Lower Rates & Equity

What if your Gilroy sanctuary could fund its own legacy through one strategic financial decision? Many homeowners in our community feel the weight of Santa Clara County’s cost of living, especially as the median home price climbed past $1.85 million in late 2025. It’s natural to feel protective of your hard-earned equity while wondering if you’re overpaying on your monthly statement. When you explore how to refinance mortgage gilroy homes this year, you aren’t just chasing a lower interest rate; you’re anchoring your family’s financial future with the integrity it deserves.

We understand that the shift in 2026 conforming loan limits to over $1.2 million can be confusing, and the anxiety surrounding hidden closing costs is valid. This guide shows you exactly how to capture lower rates, access cash for home improvements, or transition from an unpredictable ARM to a secure fixed-rate. We’ll walk through the specific local data and ethical strategies needed to make your next move a seamless part of your life’s story.

Key Takeaways

- Leverage the significant equity gains of 2024-2025 to transform your Gilroy property into a more powerful financial asset and personal sanctuary.

- Discover the strategic advantages of a refinance mortgage gilroy homeowners can use to either lower monthly payments or access liquid capital for future investments.

- Master the “break-even” calculation to ensure your transition to lower rates provides a seamless and profitable return on investment after closing costs.

- Streamline your application process by gathering essential “Integrity” documents that meet the specific standards of local Santa Clara County lenders.

- Learn why partnering with a dedicated local broker-realtor offers a sophisticated, human-centered alternative to the impersonal algorithms of national call centers.

Understanding the Gilroy Refinance Landscape in 2026

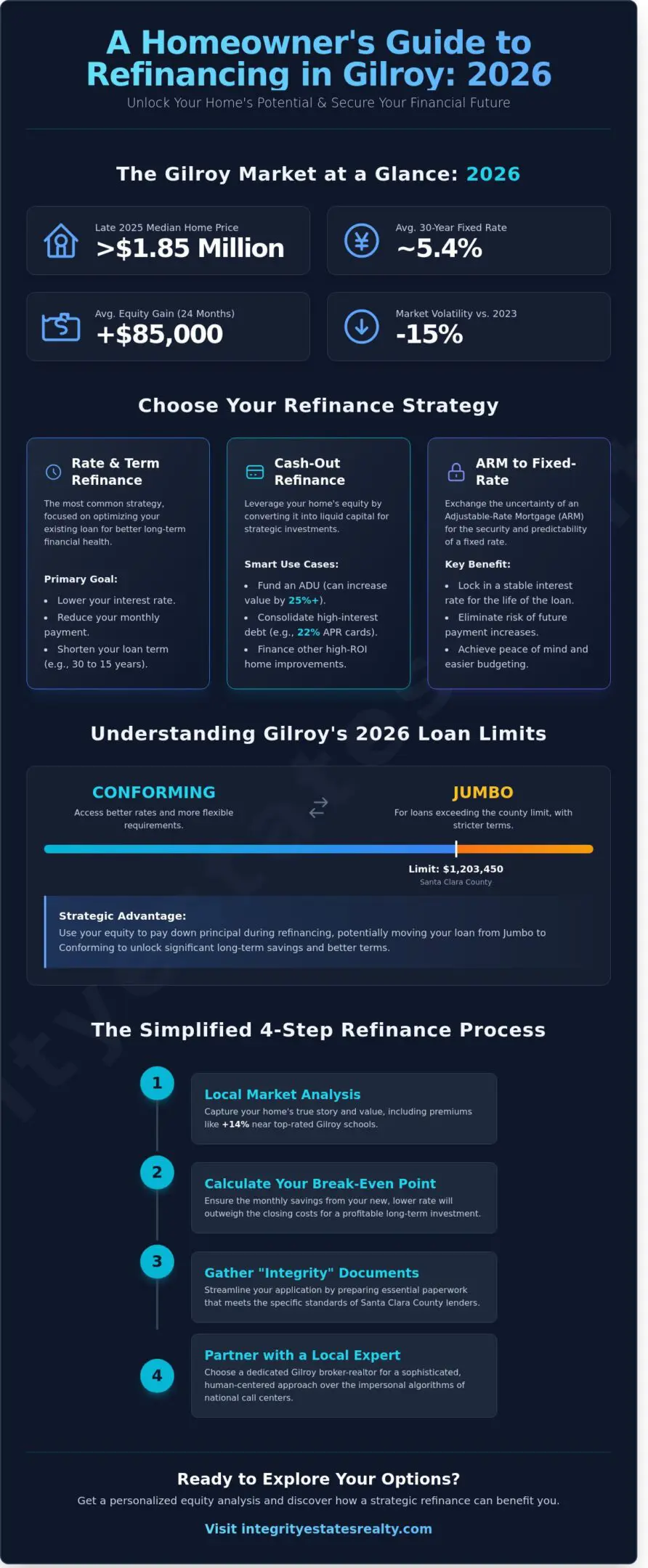

The 2026 Gilroy real estate market is no longer defined by the frantic bidding wars of the past decade. Instead, we see a landscape of mature growth where your home’s value is a testament to the community’s resilience. In Santa Clara County, interest rates have found a stable equilibrium at approximately 5.4% for a 30-year fixed mortgage, providing a predictable environment for those looking to refinance mortgage gilroy properties. This stability allows you to treat your home as both a personal sanctuary and a strategic financial asset.

Gilroy homeowners are in a unique position of strength because of the substantial equity gains realized between 2024 and 2025. During that 24-month period, local property values rose by an average of 11.2%, driven by the continued expansion of the Silicon Valley tech corridor. As more professionals seek the balance of South County living, the commute remains a primary driver of value. Understanding these gilroy real estate market trends is essential when considering refinancing in this climate, as it’s about much more than just the headline interest rate; it’s a collaborative partnership between you and the market to secure your family’s legacy and optimize your monthly cash flow.

- Market Stability: Santa Clara County’s 2026 volatility index has dropped 15% compared to 2023.

- Equity Growth: Average Gilroy equity increased by $85,000 over the last 24 months.

- Financial Integrity: Strategic refinancing focuses on total interest savings over the life of the loan.

Local Equity Trends: From Glen Loma Ranch to Downtown

Specific neighborhoods in Gilroy have outpaced state averages in appreciation, with Glen Loma Ranch seeing a 6.8% annual increase in 2025. Properties near top-rated institutions within the Gilroy Unified School District, particularly those with a GreatSchools rating of 8 or higher, have maintained a 14% appraisal premium. A precise local market analysis is the first step in any successful refinance. It allows us to capture the “story” of your home’s value, ensuring your appraisal reflects the true lifestyle curation you’ve invested in your property.

2026 Conforming vs. Jumbo Loan Limits in Gilroy

Understanding the high-cost area designations for Santa Clara County is vital for a seamless transition to a new loan. By staying within conforming limits, you can avoid the stricter debt-to-income requirements and the 0.75% rate premium often found with jumbo products. In 2026, the conforming loan limit for single-family homes in Gilroy is $1,203,450. Strategic homeowners are using their recent equity gains to pay down principal balances during the refinance process, effectively moving from jumbo territory into a conforming loan to maximize their long-term savings.

Choosing the Right Refinance Strategy for Your California Home

Selecting a path depends on your financial legacy. A refinance mortgage gilroy isn’t a one-size-fits-all solution; it’s a tool to sculpt your financial future. Whether you’re seeking to lower your monthly overhead or tap into your home’s growing equity, your choice should align with your ten-year wealth strategy. In the current 2026 market, homeowners are moving away from temporary fixes and toward structures that offer long-term sanctuary.

The rate-and-term refinance remains the most common choice for those looking to decrease their interest rate or shorten their loan duration. Moving from a 30-year to a 15-year mortgage can save hundreds of thousands in interest over the life of the loan. For those currently in an adjustable-rate mortgage, transitioning to a fixed-rate product provides peace of mind. You can consult the Federal Reserve’s guide to refinancing to understand how these structural changes impact your long-term interest costs and total loan balance. If you’re unsure which path fits your specific neighborhood, connect with our local advisors for a tailored equity analysis.

When a Cash-Out Refinance Makes Sense

Gilroy property values have seen steady growth, making equity a powerful asset for the disciplined homeowner. A cash-out refinance gilroy allows you to access this capital for high-ROI projects. Many local residents use these funds to build Accessory Dwelling Units (ADUs), which can increase property value by 25% or more while providing rental income. Others use equity to consolidate high-interest debt or explore opportunities in commercial real estate Gilroy markets where industrial expansion and retail revitalization are creating new investment opportunities. Replacing a 22% APR credit card balance with a mortgage rate significantly lower creates immediate monthly relief. To maintain a healthy financial profile, we recommend keeping your Loan-to-Value (LTV) ratio below 80%. This preserves your equity cushion and avoids the added cost of private mortgage insurance.

The FHA Streamline Advantage for Gilroy Borrowers

For those currently holding FHA & VA Loans in Gilroy, the streamline option is a gift of efficiency. It removes the hurdle of a new appraisal and skips the standard income verification process, provided you’ve stayed current on your payments for the last 12 months. This is a seamless way to lower your rate when market conditions shift in your favor. When exploring FHA home loans in Gilroy, remember the “net tangible benefit” rule. This regulation ensures the refinance mortgage gilroy provides a genuine financial gain, such as a 5% reduction in the total monthly payment. VA borrowers can enjoy similar benefits through the Interest Rate Reduction Refinance Loan (IRRRL), which prioritizes speed and simplicity for our local veterans.

Calculating the Real Cost: Is Refinancing in Gilroy Worth It?

Refinancing isn’t just about chasing a lower number on a screen; it’s a strategic realignment of your sanctuary’s financial foundation. While a lower monthly payment feels like an immediate win, the true measure of success lies in the net benefit over the remaining life of your loan. Deciding to refinance mortgage gilroy properties requires a sharp eye for detail and a commitment to long-term financial health. You’ll encounter several standard expenses during this transition. These typically include professional appraisal fees ranging from $600 to $900, title search and insurance costs, and lender origination fees that often total 1% of the loan amount. For a detailed breakdown of these expenses, the CFPB guide to home loans provides a transparent look at what homeowners should expect at the closing table.

California homeowners must also consider the tax landscape before signing new loan documents. Since the 2017 Tax Cuts and Jobs Act, interest deductions are capped on mortgage debt over $750,000. Because Gilroy home values often exceed this threshold, it’s vital to consult with a qualified CPA to ensure your new loan doesn’t inadvertently increase your tax liability or diminish the benefits of itemizing your deductions. Understanding the precise market conditions and when to refinance mortgage california properties can help you avoid costly timing mistakes that could impact your long-term financial strategy.

The Break-Even Analysis: A Gilroy Example

With the average Gilroy home value reaching approximately $1,100,000 in early 2026, the stakes for a refinance mortgage gilroy are high. Imagine your total closing costs reach $11,000 and your new rate saves you exactly $350 per month. To find your break-even point, divide the total closing costs by the monthly reduction in your mortgage payment to determine the exact number of months needed to recoup your investment. In this scenario, it takes 32 months to start seeing actual profit. You must also weigh the opportunity cost of the equity you’re utilizing. Tapping into that wealth reduces your immediate ownership stake, which could have otherwise grown through market appreciation alone without increasing your debt load.

Avoiding the ‘No-Cost’ Refinance Trap

Lenders frequently market “no-cost” options to alleviate the sting of upfront fees. These aren’t gifts; they’re trade-offs. The bank typically covers your closing costs by charging a higher interest rate, which can cost you tens of thousands of dollars over a 30-year term. True integrity in lending means showing you the math for both paths. Ask your broker for a side-by-side comparison of the total interest paid over the life of the loan. If you plan to stay in your Gilroy home for a decade or more, paying the costs upfront is almost always the more sophisticated financial move. Demand transparency regarding the par rate versus the rate offered with lender credits to ensure you’re making a choice that protects your family’s legacy.

The Step-by-Step Gilroy Refinance Process

Securing a refinance mortgage gilroy requires a methodical approach that balances financial precision with local market insight. It begins with the “Integrity” phase, where we gather your essential documentation to build a transparent profile. You’ll need your two most recent W2s, 60 days of bank statements, and tax returns from the last two years. This preparation isn’t just about paperwork; it’s about establishing the reliability that lenders demand in 2026. Before you begin, working through a comprehensive mortgage refinance checklist can help ensure no critical document or step is overlooked. As your local broker, we don’t just submit a file to a single bank. We shop your unique profile across a network of 18 wholesale lenders to find the specific pricing and terms that protect your family’s legacy.

Preparing Your Home for the Appraisal

The appraisal is a pivotal moment that determines your available equity. Small investments, like refreshing the landscaping or applying a neutral coat of paint, can increase a property’s perceived value by 3% to 7% based on recent Santa Clara County data. We recommend providing the appraiser with a curated list of every upgrade you’ve made since 2023. If the valuation comes in lower than expected, we can initiate a “rebuttal of value” using recent Gilroy “comps” that more accurately reflect your home’s worth as a sanctuary.

Underwriting in the Digital Age: Speed vs. Accuracy

Efficiency is paramount in today’s market. Many of our clients now benefit from same-day pre-approvals, allowing move-up buyers to act with the confidence of a cash offer. However, speed shouldn’t sacrifice the accuracy of your financial story. Common red flags, such as undisclosed debts or unexplained deposits over $1,000, can stall a California refinance for weeks. To stay ahead of these hurdles, review our Lower Your Rate: A Gilroy Mortgage Refinance Checklist for a complete list of required items.

The journey concludes with the closing, a moment of transition where your new financial strategy becomes reality. Once you sign the final documents at a local Gilroy title office, federal law provides a three-day right of rescission. This mandatory waiting period acts as a final safeguard, giving you 72 hours to ensure the new terms align perfectly with your long-term vision. This process is designed to be seamless, turning a complex financial move into a stress-free step toward your future goals.

Why Partner with a Local Gilroy Broker-Realtor?

Choosing to refinance mortgage gilroy properties shouldn’t feel like a transaction with an anonymous algorithm. National call centers treat your financial history as a sterile data point. At Integrity Estates Realty, we treat it as the foundation of your family’s legacy. We understand that a home in the Garlic Capital isn’t just an asset; it’s a sanctuary that requires a nuanced approach. Our deep-rooted knowledge of Santa Clara County allows us to identify lenders that specifically favor South County’s unique property values. We know which appraisers understand the difference between a suburban tract home and a custom hillside estate, ensuring your home’s equity is fully realized and protected during the appraisal process.

Broker vs. Bank: Who Wins for You?

A single bank offers one limited menu of products. We provide access to over 50 wholesale lenders simultaneously. This competitive environment ensures you secure the most aggressive rates available in the 2026 market. For the 18 percent of Gilroy residents who are self-employed or work as consultants in the nearby Silicon Valley tech corridor, traditional bank “boxes” often lead to unnecessary rejections. We specialize in complex financial files, utilizing manual underwriting to prove your stability. Our team handles the exhausting paperwork chase, often reducing the standard 45-day closing window to as little as 21 days through our dedicated local processing channels. To understand the full advantage of working with experienced mortgage brokers in Santa Clara County, including how a 0.25% rate difference can represent a $150,000 impact on your long-term wealth, our 2026 buyer’s guide to home financing provides the essential context every homeowner needs.

Your Gilroy Legacy: Beyond the Transaction

Your financial journey doesn’t end when the final documents are signed. We view ourselves as your long-term advisors, helping you bridge the gap between your current needs and future aspirations. Whether you’re tapping into equity for a sustainable home renovation, exploring commercial real estate Gilroy investment opportunities, or preparing to expand your real estate portfolio, our dual expertise as brokers and Realtors provides a comprehensive view of your wealth. We prioritize your peace of mind by ensuring every decision aligns with your long-term goals. For those planning their next move within our beautiful community, our Homes for Sale in Gilroy, CA: The 2026 Buyer’s Lifestyle & Financing Guide provides the essential insights needed for strategic planning. If you’re considering a move to maximize your equity position, our comprehensive guide on how to sell my home in Gilroy for maximum equity offers strategic insights for homeowners looking to leverage the current market conditions.

Getting started is straightforward. We offer a 15-minute strategy call to audit your current mortgage and compare it against 2026’s shifting interest rate environment. This isn’t a high-pressure sales pitch; it’s a professional consultation designed to provide clarity. We’ll examine your equity, your credit profile, and your lifestyle goals to see if a refinance mortgage gilroy plan makes sense for your specific situation. Let’s build your financial future on a foundation of local expertise and unwavering integrity.

Secure Your Financial Legacy in the 2026 Gilroy Market

Navigating the evolving landscape of 2026 requires more than just watching the news. It demands a precise understanding of your home’s current equity and the specific closing costs associated with Santa Clara County transactions. By identifying the right timing to refinance mortgage gilroy, you can potentially lower your monthly obligations and secure a more stable financial sanctuary for your family’s future. Success in this market depends on balancing technical market analysis with your personal long term goals.

Don’t leave your largest investment to chance or an impersonal algorithm. Our team brings over 20 years of Santa Clara County expertise to every consultation, offering you access to a network of 50 wholesale lenders for the most competitive rates. We operate as an independent, locally owned firm that prioritizes your peace of mind over quick sales. This collaborative approach ensures your refinance strategy aligns perfectly with your lifestyle goals and wealth building plans. You deserve a partner who is as invested in your home’s story as you are.

Schedule your free 15-minute Gilroy Refinance Strategy Call with Integrity Estates Realty and discover how we can help you turn your home into a more powerful financial asset today.

Frequently Asked Questions

How much equity do I need to refinance my home in Gilroy?

You generally need at least 20% equity to secure the most favorable interest rates and avoid the added cost of private mortgage insurance. However, specific programs allow for a refinance mortgage gilroy with as little as 3% equity for conventional loans or 0% for VA interest rate reduction loans. Maintaining a higher equity stake preserves your financial sanctuary and ensures your home remains a stable pillar of your family legacy.

Can I refinance if my credit score has dropped since I bought my house?

You can still refinance with a lower credit score, provided you meet the minimum requirement of 620 for conventional options or 580 for FHA programs. While a score drop might result in a 0.5% to 1.1% increase in your offered rate, our team works to find a path that maintains your financial integrity. We view this as a collaborative partnership to stabilize your monthly obligations despite temporary market shifts or personal transitions.

What are the current mortgage refinance rates in Santa Clara County for 2026?

Mortgage refinance rates in Santa Clara County for early 2026 are currently averaging between 5.25% and 5.85% for a 30-year fixed-rate loan. These figures represent a 0.75% decrease from the peaks seen in late 2024. Securing these rates allows Gilroy homeowners to lower their monthly overhead by approximately $350 for every $500,000 borrowed, reinforcing the long-term value of their local property investment and the story behind their front door.

How long does the mortgage refinance process usually take in California?

The mortgage refinance process in California typically spans 30 to 45 days from the initial application to the final funding date. This timeline includes a 10-day period for the property appraisal and a 5-day window for the final underwriting review. Our methodical approach ensures a seamless transition, allowing you to move through the bureaucratic requirements with the calm confidence that every detail is being handled with absolute precision.

Is it possible to refinance with a cash-out option for an ADU in Gilroy?

It’s entirely possible to utilize a cash-out refinance in Gilroy to fund an Accessory Dwelling Unit, provided you maintain at least 20% equity in your primary residence after the loan closes. In Gilroy, homeowners are using this strategy to increase their property value by an average of 22% through the addition of a secondary suite. This lifestyle curation transforms your backyard into a source of rental income or a private sanctuary for multi-generational living.

What happens to my impound account when I refinance?

Your current impound account will be closed and the remaining balance will be refunded to you by your old lender within 30 days of the loan payoff. You’ll then establish a new escrow account with your new lender to cover property taxes and homeowners insurance. This transition is a standard part of a refinance mortgage gilroy, ensuring your tax obligations are met without disrupting your personal peace of mind or financial rhythm.

Can I refinance my mortgage if I have a second lien or HELOC?

You can refinance your first mortgage even with a second lien or HELOC, though the secondary lender must agree to a resubordination agreement. This legal document keeps the second loan in its current priority position behind the new primary mortgage. Approximately 18% of our clients choose to roll their HELOC into a new primary loan to consolidate debt into a single, predictable monthly payment that supports their long-term wealth.

How often can I refinance my mortgage in California?

California law doesn’t set a hard limit on frequency, but most lenders require a seasoning period of 6 to 12 months between transactions. We evaluate each opportunity based on a net tangible benefit test to ensure the move saves you at least 0.5% in interest or reduces your loan term significantly. Our goal is to act as your steadfast guide, ensuring every financial decision serves your future with the honesty and transparency you deserve.