Low Down Payment Homes in Hayward, CA: Your 2026 Path to Homeownership

What if you could secure a home in the East Bay without a six-figure savings account, even while competing against aggressive all-cash investors? In a market where the median home price currently ranges from $809,000 to $862,000, finding low down payment homes hayward ca requires more than just luck; it requires a sophisticated financial strategy. You likely feel the weight of recent data showing that 70.3% of local homes sell above their list price, making the dream of homeownership feel like a moving target.

We understand that the high cost of living in Alameda County creates a significant barrier for even the most diligent savers. This guide provides a definitive roadmap to purchasing a property with as little as 0% to 3.5% down by leveraging specific FHA and VA loan programs tailored to your needs. You’ll learn how to navigate the current 30-year fixed interest rates of 6.33% to 6.49%, determine if your household qualifies for assistance based on the $155,700 area median income, and identify upcoming deadlines for city-specific BMR units. We’ll explore the layering of mortgage options and local incentives to ensure you move forward with clarity and confidence.

Key Takeaways

- Learn why a 20% down payment is no longer a requirement for entering the East Bay market and how alternative strategies can accelerate your path to ownership.

- Explore the nuances of FHA and VA loan originations that allow qualified buyers to purchase with as little as 0% to 3.5% down in Alameda County.

- Uncover the “layering” method to find low down payment homes hayward ca by combining specific mortgage products with local BMR opportunities.

- Gain a clear understanding of the application windows for local housing programs to ensure you are prepared when new funding cycles open.

- Discover how integrated real estate and mortgage expertise provides a competitive edge when negotiating in Hayward’s fast-moving neighborhoods.

Navigating the Hayward Real Estate Market with Low Down Payment Strategies

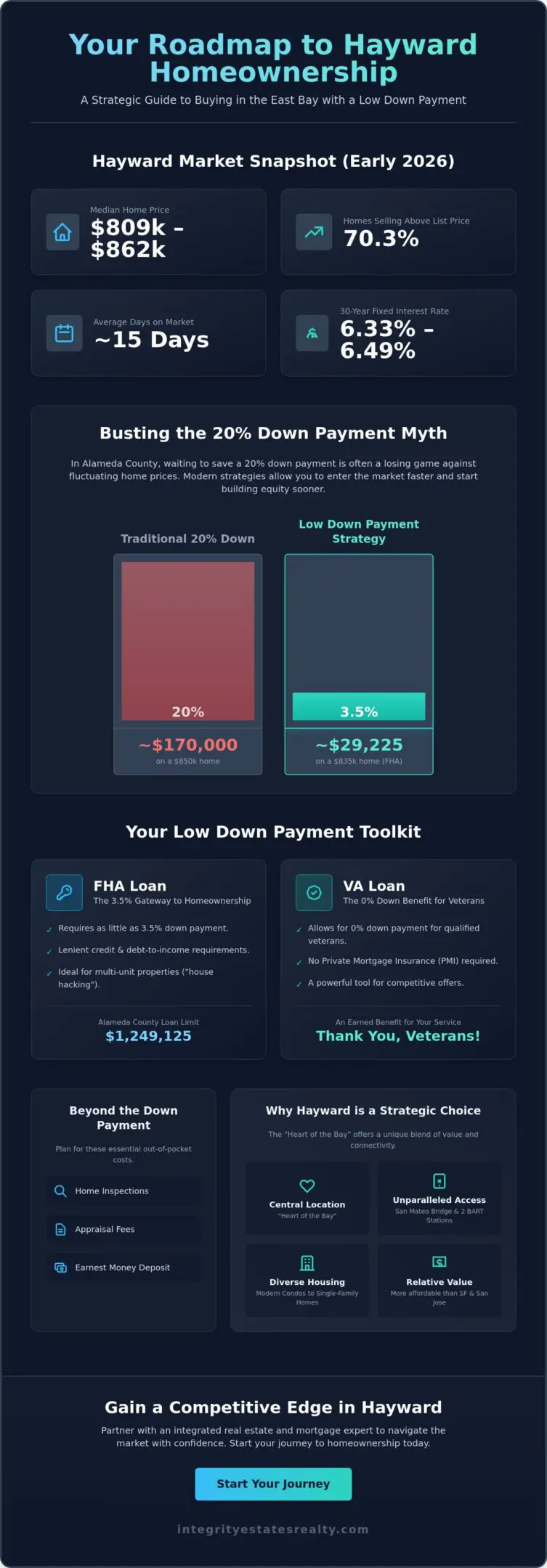

The Hayward housing market in early 2026 presents a unique opportunity for those who feel priced out of the surrounding Silicon Valley. While the median home price sits between $809,000 and $862,000, the market has seen a slight 4.1% cooling compared to the previous year. This shift doesn’t mean competition has vanished. Homes still sell in about 15 days on average, and over 70% of transactions close above the list price. However, it does mean that buyers who focus on low down payment homes hayward ca can find an entry point that didn’t exist during the height of the recent price surges.

Moving past the 20% down payment myth is the first hurdle for many East Bay families. In a high-cost area like Alameda County, waiting to save $170,000 while prices continue to fluctuate is often a losing game. Modern lending allows you to preserve your liquidity. By utilizing 3.5% or 0% down options, you keep your capital available for life’s other necessities while building equity in a permanent asset. We view this as a strategic move to hedge against future inflation while securing your place in a desirable region.

Why Hayward is the Strategic Choice for East Bay Buyers

Hayward is often called the “Heart of the Bay” for good reason. Its location offers unparalleled access to major employment hubs via the San Mateo Bridge and two BART stations. You’ll find a diverse inventory here that neighboring cities like San Leandro or Union City often lack. From modern condos in South Hayward to established single-family residences in the Hayward Hills, the variety supports different lifestyle needs. While San Jose and San Francisco prices remain astronomical, Hayward offers a relative value play without sacrificing the urban connectivity required for a modern career.

The Reality of Down Payments in 2026

The 2026 conforming loan limit for a one-unit property in Alameda County is $1,249,125. This high ceiling allows you to shop for substantial homes using low-down-payment financing. It’s a vital tool when 30-year fixed rates hover between 6.33% and 6.49%. In this environment, your strategy should focus on the total monthly obligation rather than just the initial check. Securing low down payment homes hayward ca requires a partner who understands how to balance these interest rates with your long-term financial health.

You also need to distinguish between your down payment and your “cash-on-hand.” Even with a 0% down VA loan, you’ll need funds for specific out-of-pocket costs. These typically include:

- Professional home inspections to ensure the property’s structural integrity.

- Appraisal fees required by the lender to verify the home’s value.

- Earnest money deposits to demonstrate your commitment to the seller.

Planning for these smaller outlays ensures your journey remains smooth and predictable. We prioritize transparency in these details so you aren’t surprised by the logistics of the transaction.

Mortgage Programs for Buying a Home with Minimal Cash Out-of-Pocket

Securing a property in the East Bay doesn’t require a massive upfront investment if you select the right financing vehicle. While the market remains competitive, the variety of loan products available in 2026 allows for significant flexibility. Most buyers seeking low down payment homes hayward ca utilize programs that trade a smaller initial payment for mortgage insurance. This insurance protects the lender, but for you, it serves as the key that unlocks the door to homeownership years sooner than traditional saving methods would allow.

FHA Loans: The 3.5% Gateway to Hayward Homeownership

The FHA loan remains a cornerstone for local buyers due to its lenient credit requirements and low 3.5% down payment. In 2026, the high-cost loan limits for Alameda County align with the conforming limit of $1,249,125, providing ample room to finance even larger single-family homes. FHA guidelines are particularly helpful if your debt-to-income ratio is slightly higher or if your credit history has minor blemishes.

Many of our clients use FHA financing to purchase multi-unit properties, such as a duplex or fourplex. You can live in one unit while using the rental income from the others to help qualify for the mortgage. This “house hacking” strategy is a sophisticated way to build wealth in Hayward while keeping your initial cash outlay to a minimum. It’s a practical path for those who want their asset to work for them from day one.

VA Loans: 0% Down for Hayward’s Military Families

For those who have served, the VA loan is arguably the most powerful financial tool in real estate. It offers a 0% down payment and, unlike other low-down-payment options, requires no monthly mortgage insurance. This “No-No” deal significantly reduces your monthly obligation compared to FHA or conventional loans.

When shopping for older homes in established Hayward neighborhoods, be mindful that VA appraisals focus heavily on safety and structural integrity. We guide our veteran clients through this process to ensure the property meets these rigorous standards before closing. If you’re considering expanding your search to nearby regions, our Mortgage Brokers in Santa Clara County can help you compare how these benefits apply across county lines.

Conventional 3% and First-Time Buyer Incentives

If you have a credit score of 720 or higher, a Conventional 97 loan might be your best option. Programs like Fannie Mae’s HomeReady or Freddie Mac’s Home Possible allow for a 3% down payment. These programs often feature reduced mortgage insurance costs, especially if your household income is below the 2025 Area Median Income of $155,700 for Alameda County. We can help you analyze your specific census tract to see if you qualify for these specialized incentives. If you’re ready to see which program fits your financial profile, you can explore our mortgage services to begin your pre-approval journey.

Hayward-Specific Programs: BMR vs. Down Payment Assistance (DPA)

Securing a property in the East Bay often requires a multi-layered financial strategy. While the mortgage products discussed earlier provide the foundation, local incentives can further lower the barrier to entry. You’ll generally choose between two distinct paths: purchasing a Below Market Rate (BMR) unit or utilizing Down Payment Assistance (DPA) on a market-rate home. Each option carries unique implications for your monthly budget and your long-term wealth accumulation. Finding low down payment homes hayward ca often depends on how well you align these programs with your specific household income and residency goals.

Understanding Hayward’s Below Market Rate (BMR) Program

The City of Hayward periodically offers BMR units, which are homes priced significantly below the market median to remain affordable for moderate-income households. These opportunities are development-specific. For instance, in early 2026, application deadlines for the La Vista development were set for May 21, while the Depot Community Apartments accepted applications through June 8. To qualify, you must meet the “first-time buyer” definition, meaning you haven’t owned a primary residence in the last three years.

Eligibility is typically tied to the Area Median Income (AMI). For 2025, the AMI for a four-person household in Alameda County was $155,700. While BMR units offer an accessible entry point, they come with a significant trade-off: limited equity growth. Resale restrictions ensure the home remains affordable for the next buyer, which means you won’t capture the full market appreciation. It’s a choice between immediate affordability and the aggressive wealth building found in traditional real estate.

California State DPA Grants and Forgivable Loans

If you prefer a market-rate home to capture full appreciation, state-level assistance can bridge the gap. The CalHFA MyHome Assistance Program provides a deferred-payment junior loan that can cover your down payment or closing costs. Additionally, the Forgivable Equity Builder Loan offers a path where the debt may be forgiven if you remain in the home for a specified period, typically five years.

It’s important to note that the popular “Dream For All” shared appreciation loan window for 2026 closed in mid-March. Buyers must now look toward other steady programs or wait for future funding cycles. If you find that Hayward’s price points remain a challenge even with these grants, you might compare these options with FHA Home Loans in Gilroy to see how regional inventory and affordability differ. Choosing the right program is a collaborative process, and we’re here to help you weigh the pros and cons of each path to ensure your move into low down payment homes hayward ca is both ethical and financially sound.

Ultimately, the decision rests on your timeline. DPA programs on market-rate homes allow for greater mobility and profit when you eventually sell. BMR units, conversely, provide a sense of permanence and lower monthly housing costs in a city where 70.3% of homes recently sold above their asking price. We prioritize your peace of mind by analyzing these nuances before you sign a contract.

How to Successfully Secure Low Down Payment Homes in Hayward

Winning a home in the East Bay requires more than just a pre-approval letter; it demands a tactical approach to the offer process. In a market where homes sell in an average of 15 days and 70.3% of properties close above the list price, your strategy must be precise. Successfully finding low down payment homes hayward ca involves identifying the right inventory and presenting yourself as a low-risk buyer to sellers who are often distracted by the allure of all-cash offers. We focus on building a comprehensive financial profile that demonstrates your stability and readiness to close, regardless of your down payment size.

Identifying High-Potential Properties for Low-Down Financing

Your search should prioritize properties that align with the specific requirements of FHA and VA appraisals. Condos and townhomes in neighborhoods like Tennyson-Alquire often serve as excellent starter assets because they frequently meet the structural standards required for low-down-payment financing. When viewing older single-family homes, look for “un-financeable” conditions such as peeling paint, dry rot, or outdated electrical systems. These issues can stall an FHA or VA loan during the inspection phase, so identifying them early saves time and emotional energy.

Leverage is another critical factor. While the broader Hayward market is fast-moving, focusing on listings with more than 30 days on the market can provide significant negotiation room. Sellers of these properties are often more willing to entertain offers with lower down payments or those requesting specific contingencies. This patience allows you to avoid the 15-day “feeding frenzy” and secure a property on terms that protect your liquidity.

Negotiating Seller Credits to Cover Closing Costs

One of the most effective ways to preserve your cash-on-hand is through the “Gross-Up” strategy. This involves offering a slightly higher purchase price while requesting a corresponding seller credit to cover your closing costs. For example, if a home is listed at $820,000, you might offer $830,000 with a $10,000 credit back to you at close of escrow. This effectively finances your closing costs into the mortgage, keeping thousands of dollars in your bank account for future home improvements or emergencies.

Pitching a low-down-payment offer as “low risk” requires a partner who can communicate your financial strength to the listing agent. We emphasize your debt-to-income ratios and the thoroughness of your in-house mortgage processing to reassure the seller. By providing a net sheet that shows exactly what the seller will walk away with, we remove the ambiguity that often plagues these transactions. If you’re ready to build a winning offer strategy, you can schedule a consultation for our residential representation services to begin your search.

Our dual-licensed expertise allows us to calculate these complex financial maneuvers on the fly during a showing. This agility ensures that when you find the right home, your offer is both competitive and protective of your long-term wealth. We treat every transaction as a collaborative partnership, guiding you through the nuances of the Hayward landscape with professional composure.

Partnering with a Combined Real Estate and Mortgage Brokerage

The complexity of securing low down payment homes hayward ca requires a level of coordination that traditional, fragmented real estate models simply cannot provide. When your real estate representative and your loan officer work under the same roof, the friction that often leads to delayed closings or missed opportunities disappears. We offer a unified approach where residential real estate representation and in-house mortgage services, including FHA and VA loan originations, function as a single, cohesive unit. This integration ensures that every financial detail of your offer is verified and communicated with absolute precision to the listing agent.

Nena Arriaga brings over 20 years of experience to this collaborative process, providing a depth of local knowledge that is essential in Hayward’s competitive environment. Her tenure in the East Bay allows her to anticipate market shifts and negotiate terms that protect your interests while maximizing your purchasing power. This isn’t just about a transaction; it’s about a long-term partnership rooted in ethical conduct and a shared vision for your future. Our regional expertise extends across the Bay, and you can see our broader perspective in our analysis of Gilroy Real Estate Market Trends.

The Efficiency of Streamlined Financing and Representation

Eliminating the middleman between your agent and lender is a significant advantage when time is of the essence. In a market where homes often sell in just 15 days, waiting for an outside lender to update a pre-approval letter can cost you the property. We provide real-time updates as you tour homes, allowing us to adjust your strategy based on the specific nuances of a listing. This agility is particularly vital when competing for low down payment homes hayward ca, as it proves to the seller that your financing is robust and ready for execution.

Your Next Steps to Homeownership in Hayward

Your journey begins with a comprehensive portfolio review. We’ll analyze your income, current debt, and long-term goals to determine which mortgage program, whether FHA, VA, or Conventional, best serves your needs. To prepare for this session, you’ll want to gather your essential “Integrity” documents, including recent tax returns, paystubs, and bank statements. Having these ready allows us to move with the intentional, calm pace required for success in 2026.

Our goal is to alleviate the stress of high-stakes transactions through transparency and expert guidance. By focusing on lifestyle curation and your personal narrative, we bridge the gap between a physical asset and your personal dream. Contact Integrity Estates Realty today to schedule your Hayward-specific strategy session and take the first step toward securing your future in the East Bay.

Your Future in the East Bay Begins Today

Achieving homeownership in the Heart of the Bay is a matter of strategic alignment rather than just luck. You’ve discovered how specialized mortgage products and local incentives like Hayward’s BMR units can significantly lower your entry barrier. Success in this competitive landscape depends on acting with precision and confidence. With the local market moving at a pace of 15 days per sale, having your financing and representation synchronized is the most effective way to secure low down payment homes hayward ca.

At Integrity Estates Realty, we bring over 20 years of California real estate experience to your side. As a dual-licensed brokerage, we provide a streamlined path through FHA loan originations, VA benefits, and complex DPA programs. This integrated expertise ensures your offer is both financially sound and attractive to sellers. We’re ready to help you navigate these nuances with the transparency and peace of mind you deserve. Our role is to serve as your steadfast guide, bridging the gap between a physical asset and your personal dream.

Start your Hayward home search with a free mortgage and real estate consultation. The door to your new East Bay lifestyle is open, and we’re here to walk through it with you.

Frequently Asked Questions

Can I really buy a home in Hayward with 0% down?

Yes, qualified veterans and active-duty service members can utilize VA loan originations to purchase a property with zero money down. While state-level programs like “Dream For All” had specific windows that closed in March 2026, other local grants and forgivable loans occasionally become available to bridge the gap for non-military buyers. We focus on identifying these specific vehicles to help you secure low down payment homes hayward ca without needing a massive cash reserve.

What is the maximum loan limit for FHA in Hayward for 2026?

The 2026 FHA loan limit for a one-unit property in Alameda County is $1,249,125. This generous ceiling allows you to apply 3.5% down payment strategies to a wide variety of single-family homes and even some luxury condos. Because Hayward’s median home prices currently sit between $809,000 and $862,000, most available inventory falls well within these FHA financing guidelines.

Do I have to be a first-time homebuyer to use down payment assistance?

Most programs don’t require you to be a “true” first-time buyer; instead, they require that you haven’t owned a primary residence in the last three years. If you’ve been renting for at least 36 months, you generally qualify for the same incentives as someone who has never owned a home. This definition opens the door for many former homeowners to re-enter the Hayward market using low-down-payment strategies.

How much are closing costs typically for a home in Hayward?

Closing costs in the East Bay generally range from 2% to 5% of the total purchase price. These costs include essential items like title insurance, escrow fees, and professional appraisals. We often utilize the “Gross-Up” negotiation strategy to request seller credits, which can effectively cover these out-of-pocket expenses and preserve your liquidity during the move-in process.

Can I use a low down payment loan for a condo or townhouse in Hayward?

You can use FHA, VA, or Conventional 3% loans for condos and townhouses, provided the homeowners association (HOA) meets specific lender requirements. These properties are frequently the most affordable low down payment homes hayward ca because of their lower price points compared to detached houses. We prioritize verifying the FHA or VA “approved list” status for any complex you’re considering to ensure your financing remains secure.

Is the Hayward BMR program better than an FHA loan?

The “better” option depends entirely on whether you prioritize immediate affordability or long-term wealth building. The Hayward Below Market Rate (BMR) program offers homes at a deep discount, but resale restrictions mean you won’t capture the full market appreciation. An FHA loan allows you to buy a market-rate home where you own 100% of the equity growth, which is a significant advantage in a city where 70.3% of homes recently sold for above the list price.

How long does it take to get pre-approved for a low-down-payment loan?

A comprehensive pre-approval typically takes 24 to 48 hours once you submit your paystubs, tax returns, and bank statements. In a market where the average home sells in just 15 days, having this documentation ready is a critical competitive advantage. Our in-house mortgage processing allows us to move quickly, ensuring you’re prepared to submit a winning offer the moment you find the right property.