Mortgage Broker vs. Bank in San Francisco: Making the Strategic Choice in 2026

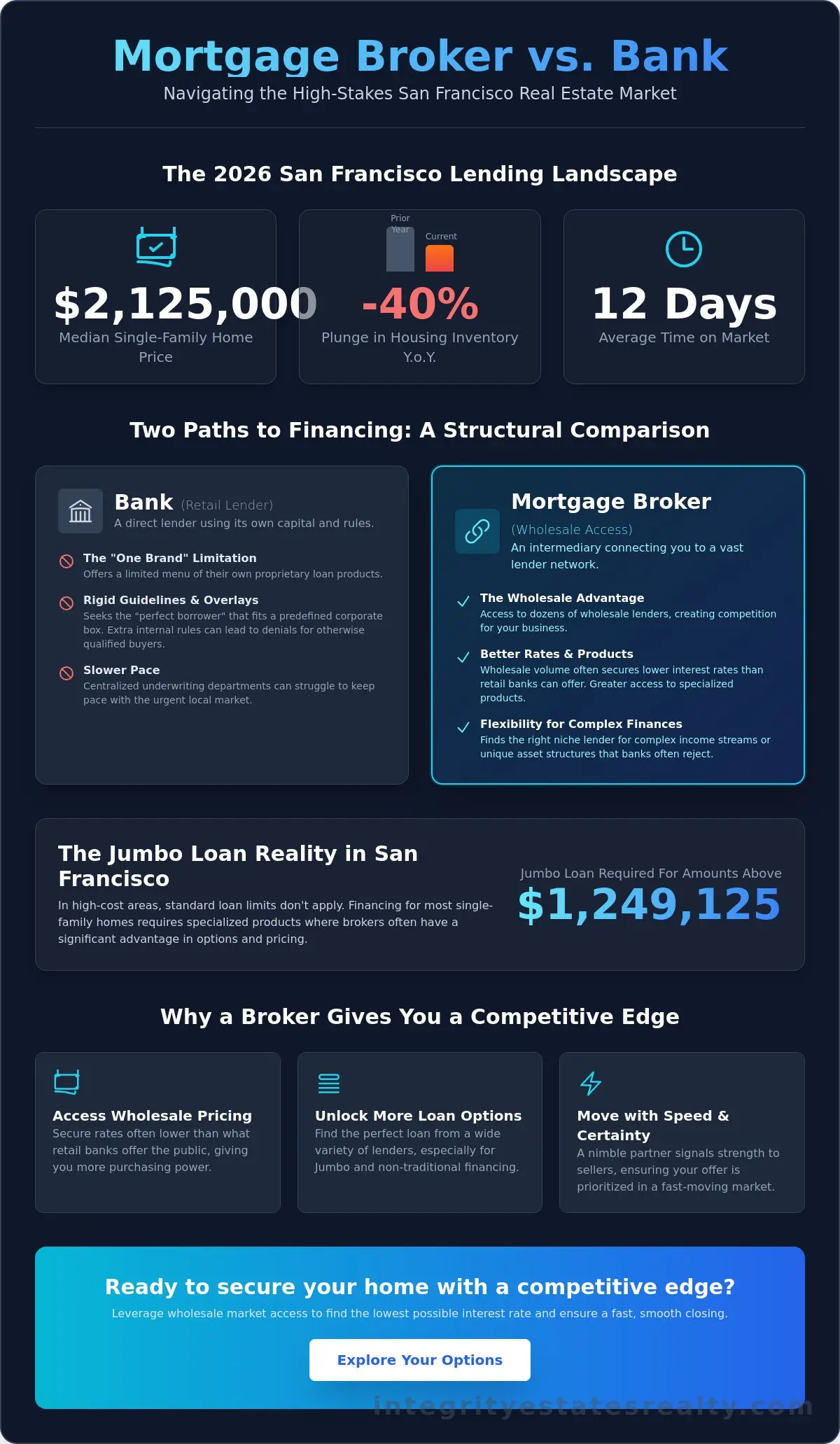

The bank you’ve used for a decade might feel like the safest harbor, but in a city where single-family homes now command a median price of $2,125,000, that loyalty could be your most expensive mistake. When weighing a mortgage broker vs bank san francisco buyers often find that the rigid structures of retail lenders simply can’t keep pace with a market where inventory has plunged by 40% year-over-year. You likely feel the weight of this intense seller’s market, where homes vanish in an average of 12 days and multiple offers are the standard. It’s natural to worry about missing the most competitive interest rate or getting buried in paperwork while a swifter, more agile buyer secures your dream property.

This guide will help you navigate these high stakes by revealing how to leverage wholesale market access to secure the lowest possible interest rate and a fast closing. We’ll explore the strategic nuances of jumbo loans, which are now the standard for our region since any loan amount above $1,249,125 requires specialized products. You’ll gain a clear understanding of the differences between these two paths so you can choose a partner who values your peace of mind and understands the unique pulse of our local culture. We’re here to help you bridge the gap between a complex financial asset and the personal dream of owning a home in the city.

Key Takeaways

- Gain clarity on how the rapid pace of the 2026 market transforms your choice of lender into a pivotal competitive advantage for securing a home.

- Uncover the structural advantages of a mortgage broker vs bank san francisco to access wholesale pricing that often undercuts standard retail rates.

- Master the nuances of Jumbo Loan origination and high-cost area limits to ensure your financing matches the reality of San Francisco property values.

- Learn the essential steps for vetting a partner’s local experience and California licensing to protect your investment and peace of mind.

- Explore how a collaborative, dual-licensed approach to real estate and lending streamlines the journey from your initial pre-approval to a successful closing.

Navigating the 2026 San Francisco Lending Landscape

San Francisco’s real estate environment in 2026 isn’t just competitive; it’s a test of strategic preparation. With the median price for a single-family home reaching $2,125,000 as of April 2026, the financial stakes have never been higher. For many buyers, the journey begins with excitement but quickly shifts into anxiety as they face a 40% decline in available inventory. This scarcity means that when you find a property, your choice of financing partner is just as critical as the home itself. Understanding the nuances of a mortgage broker vs bank san francisco can be the difference between a rejected offer and a set of keys.

The High Stakes of San Francisco Real Estate

Sellers in the Bay Area are looking for certainty. When a home stays on the market for an average of only 12 days, listing agents prioritize offers backed by lenders who can move with precision. “Big-box” retail banks often struggle with this pace. Their rigid, centralized underwriting departments can feel detached from the local urgency. In contrast, expert financing acts as a signal of strength. A lender with a deep understanding of local price floors ensures that your appraisal and funding processes don’t stall. This reliability transforms the homebuying experience from a frantic race into a composed, strategic pursuit. It’s about more than just numbers; it’s about having a partner who is as invested in your future as you are.

Broker vs. Bank: A Quick Definition

Choosing your path requires a clear understanding of how these institutions operate. Traditional banks are retail lenders. They use their own capital and offer a limited menu of internal products, which might not always fit the complex needs of a high-net-worth SF buyer. On the other hand, What is a Mortgage Broker? A broker acts as a professional intermediary, connecting you to an expansive network of wholesale partners. This model is becoming the standard in high-cost California counties because it allows for more flexibility and access to specialized Jumbo Loan products. When comparing a mortgage broker vs bank san francisco residents often find that the broker’s ability to shop dozens of lenders provides a significant edge in both rate and product variety. This collaborative approach ensures that your financing is curated to match your personal narrative and long-term financial logic.

Structural Differences: Mortgage Broker vs. Bank

Deciding on the right financing path requires more than just comparing interest rates; it requires an understanding of how these institutions are built. When evaluating a mortgage broker vs bank san francisco, you’re choosing between a retail environment and a wholesale marketplace. A bank operates as a direct lender, using its own capital and following a single set of internal rules. A broker, however, serves as a professional navigator who matches your specific financial profile with dozens of wholesale partners, many of whom don’t even have public-facing storefronts.

The “One Brand” Limitation of Banks

Banks are inherently limited by their own proprietary guidelines and risk appetite. They often look for the “perfect borrower” who fits neatly into a pre-defined corporate box. If your financial situation involves complex income streams or unique asset structures, you might encounter rigid corporate overlays. These are additional requirements that banks layer on top of standard federal guidelines, which can lead to a sudden denial even if you’re otherwise qualified. This lack of flexibility can be particularly frustrating in a high-stakes market where every delay puts your earnest money at risk.

The Wholesale Advantage of Brokers

Brokers offer a more collaborative and expansive approach. By shopping your file to multiple lenders simultaneously, they create a competitive environment where lenders vie for your business. This model provides several key benefits:

- Broad Market Access: Brokers connect you to niche lenders that specialize in specific property types or borrower profiles that traditional banks might avoid.

- Wholesale Pricing: Because brokers work at wholesale volume, they often secure rates that are lower than what a retail bank offers to the general public.

- Strategic Buffering: Wholesale rates provide a buffer against SF price volatility.

There’s a common misconception that working with an intermediary adds an unnecessary layer of cost. In 2026, the “middleman” myth is easily debunked by looking at modern compensation structures. Most brokers are paid by the lender, not the borrower, ensuring that their services remain accessible while they focus on finding the most competitive terms for your residential real estate representation. This transparency allows you to focus on the long-term value of your home rather than worrying about hidden fees. By choosing a partner who can navigate “tricky” financial profiles with ease, you gain the peace of mind necessary to act decisively in San Francisco’s fast-moving market.

Why San Francisco Buyers Need Specialized Mortgage Products

San Francisco’s real estate market operates on a different financial plane than most of the country. With the median price for a single-family home reaching $2,125,000 and condos averaging $1,400,000 as of April 2026, standard lending products often fall short. Financing these assets requires more than a simple application; it requires a strategic understanding of high-balance limits and unique property types. When comparing a mortgage broker vs bank san francisco, the choice usually hinges on who can provide the most agile solution for these high-value transactions.

Jumbo Loans and High-Balance Limits

In 2026, the conforming loan limit for a one-unit property in San Francisco County is $1,249,125. Any amount borrowed beyond this threshold is classified as a Jumbo loan. Because these loans cannot be sold to Fannie Mae or Freddie Mac, lenders must keep them on their own books or sell them to private investors. National banks often have very rigid internal “appetites” for Jumbo risk, which can lead to higher interest rates or stricter down payment requirements. Brokers often have access to more aggressive Jumbo pricing because they shop your file to dozens of wholesale partners simultaneously. This competition allows for more flexible debt-to-income (DTI) ratios, which is vital for professionals whose wealth might be tied up in restricted stock units or complex bonus structures.

FHA and VA Opportunities in High-Cost Areas

While many associate government-backed loans with entry-level markets, they remain powerful tools in high-cost regions. You can utilize FHA home loans in Gilroy and San Francisco to secure lower down payments even on high-balance properties. Brokers excel here by finding lenders who specialize in these high-limit government products, ensuring you don’t miss out on competitive rates simply because your loan amount is substantial. Local expertise is essential for navigating California-specific requirements, especially when dealing with the city’s unique property landscape.

San Francisco is famous for its Tenancy-in-Common (TIC) units and mixed-use spaces, which many traditional banks refuse to finance. These properties often present appraisal hurdles that can derail a transaction if not handled with care. A broker’s deep relationships with local appraisers and niche lenders can be the deciding factor in these complex scenarios. They act as a steadfast guide, ensuring that the technical details of the property don’t stand in the way of your personal narrative and long-term investment goals. By prioritizing specialized products over one-size-fits-all solutions, you secure a path to homeownership that is as unique as the city itself.

How to Choose the Right Lending Partner in the Bay Area

Selecting your financial partner is a decision that carries long-term weight. In a city where homes sell in an average of 12 days, you can’t afford a lender who operates on a generic national timeline. When you compare a mortgage broker vs bank san francisco specialists, focus first on their California licensing and NMLS credentials. Beyond basic compliance, you need a partner who understands the intricate nuances of local property types. Whether you’re eyeing a luxury condo or a single-family home, your lender must demonstrate a track record of closing complex transactions in the Bay Area’s high-pressure environment.

Transparency is the cornerstone of a reliable partnership. Request a comprehensive breakdown of all estimated closing costs early in the process. In San Francisco, these costs typically range from 2% to 5% of the purchase price. On a median-priced home of $2,125,000, that’s a significant investment. Don’t just look at the interest rate. Evaluate the “Total Cost of Loan” over five and ten years. This calculation includes origination fees, which generally fall between 0.5% and 1% of the loan amount. A slightly lower rate might be offset by higher upfront costs; a methodical comparison is essential for your peace of mind.

Questions to Ask Every Potential Lender

A sophisticated buyer asks pointed questions to gauge a lender’s operational efficiency. Use these inquiries to filter for quality:

- “How many wholesale lenders do you currently work with?” This reveals the actual depth of their market access.

- “What is your typical turnaround time for a Jumbo loan appraisal in SF?” Speed is your greatest asset in a multi-offer scenario.

- “Can you provide a mortgage refinance checklist for future rate drops?” A partner should be invested in your long-term financial health, not just a single transaction.

Reading Between the Lines of Reviews

Online testimonials offer a glimpse into the client experience, but they require careful interpretation. Distinguish between a mention of a “good rate” and “exceptional service.” A “good rate” is a commodity; “exceptional service” means the lender solved a problem when a deadline was looming. While you are searching in the city, the value of a broker who understands the broader region, including Gilroy real estate market trends and San Jose inventory shifts, cannot be overstated. This regional expertise suggests a deep-rooted reliability that transcends a single zip code. If you are ready to secure a strategic advantage in this market, start your journey with expert residential real estate representation today.

The Integrity Advantage: Merging Real Estate and Mortgage Expertise

San Francisco’s market demands more than just a transaction; it requires a synchronized strategy. In the traditional homebuying model, a disconnect often exists between the real estate agent and the lender, leading to misaligned timelines and unnecessary stress. Integrity Estates Realty bridges this gap through a dual-licensed approach that treats your financing and your property search as a single, cohesive journey. When you weigh the options of a mortgage broker vs bank san francisco, consider the value of a partner who understands the nuances of the local culture and the technicalities of the loan simultaneously. This integrated model provides an ethical anchor in a competitive industry, prioritizing your peace of mind over a quick closing.

Efficiency Through Integration

The path to homeownership involves significant documentation and rigorous requirements. By housing both real estate representation and mortgage expertise within one team, we drastically reduce paperwork fatigue. You won’t find yourself repeating your financial narrative to multiple parties who aren’t on the same page. This synergy ensures that when you place an offer on homes for sale in Gilroy or a condo in Pacific Heights, your bid is backed by a solid, verified financial foundation. There’s a distinct strategic benefit when your lender knows the specific history and appraisal hurdles of the house you’re buying. It allows us to move with the intentionality and speed required to win in a market where inventory is scarce and competition is fierce.

Your Partner for the Long Term

Our commitment to your future extends far beyond the day you receive your keys. We view real estate as a tool for lifestyle curation and long-term wealth building, not just a physical asset. This means we remain a steadfast guide, monitoring market shifts and interest rate movements long after the initial transaction is complete. When the economic climate shifts, we’re ready to help you refinance your mortgage in Gilroy or San Francisco to capture better terms or pull equity for future investments. Integrity is a partnership, not just a service provider. By merging local roots in Gilroy with deep expertise in the San Francisco landscape, we offer a superior service model that values the human experience behind every property. We’re as invested in your long-term success as you are, ensuring that every financial decision aligns with your personal dreams and financial logic.

Securing Your Legacy in the City

The decision between a mortgage broker vs bank san francisco represents more than a simple financial choice; it’s a strategic move to protect your investment in one of the world’s most dynamic markets. You’ve seen how wholesale access and specialized Jumbo loan products provide the necessary leverage to navigate high property values and intense competition. By prioritizing a partner who understands the local culture and the technical nuances of San Francisco real estate, you shift from a position of anxiety to one of strategic confidence. Speed, transparency, and deep market knowledge are the pillars that will support your transition from a physical asset to a personal dream.

With over 20 years of California real estate and mortgage experience, we offer an ethical partnership rooted in local pride and professional excellence. Our independently owned team provides access to a vast network of wholesale lenders, ensuring you receive the most competitive Jumbo rates available in 2026. We’re here to guide you through every complex detail with the care of a personal advisor and the authority of a market expert. Your journey toward a successful closing starts with a plan tailored specifically to your financial narrative.

Get a Personalized San Francisco Mortgage Strategy from Integrity Estates Realty

We look forward to helping you build your future in the city with peace of mind and professional integrity. You’ve got the vision; we’ve got the map to get you there.

Frequently Asked Questions

Is it better to use a mortgage broker or a bank in San Francisco?

The choice depends on your financial complexity, but a broker often provides a significant edge in our local market. While banks serve clients with simple profiles and existing accounts, brokers offer the flexibility needed for the city’s high property values. They act as a strategic navigator, accessing wholesale markets that provide more diverse product options than a single retail institution can offer.

Do mortgage brokers in California charge higher fees than banks?

Brokers don’t necessarily cost more than banks; in fact, they are often paid directly by the lender rather than the borrower. Loan origination fees across the industry generally range from 0.5% to 1% of the loan amount. Working with a broker allows you to compare these costs across multiple lenders simultaneously, ensuring you receive a transparent and competitive fee structure.

Can a mortgage broker help me get a Jumbo loan in the Bay Area?

Yes, brokers specialize in Jumbo Loan Origination, which is essential since the 2026 conforming limit in San Francisco is $1,249,125. Because brokers maintain relationships with niche wholesale lenders, they can often find more aggressive pricing and flexible debt-to-income requirements. This is a vital advantage for buyers purchasing properties that far exceed standard loan limits.

How long does it take to close a home loan with a broker vs a bank?

Brokers often facilitate a faster closing process because they work with wholesale underwriters who are used to high-volume, efficient turnarounds. In a market where homes sell in an average of 12 days, speed is a necessity. While traditional banks may struggle with internal bureaucracy, a localized broker focuses on the agility required to keep your offer competitive.

Will a broker get me a better interest rate than my personal bank?

A broker can often secure a more favorable rate by shopping your file to dozens of competing lenders. When evaluating a mortgage broker vs bank san francisco buyers frequently find that wholesale rates are lower than retail bank offers. This happens because wholesale lenders don’t carry the high overhead costs of maintaining physical bank branches, passing those savings to you.

What credit score do I need for a San Francisco mortgage in 2026?

You generally need a score of at least 700 to 720 for conventional financing, though Jumbo loans often require 740 or higher. While FHA and VA programs offer paths for those with lower scores, a higher credit profile is your best tool for securing the lowest possible interest rate. This ensures your monthly payments remain manageable despite the city’s high entry prices.

Can I switch from a bank to a broker during the home-buying process?

You can switch lenders, but doing so during an active escrow requires extreme caution to avoid missing contract deadlines. It is always best to finalize your lending partner before you start submitting offers on properties. Making the strategic choice early ensures that your pre-approval is solid and your path to closing remains smooth and predictable.

How do I verify if a San Francisco mortgage broker is licensed?

You can verify any broker’s credentials through the Nationwide Multistate Licensing System (NMLS) Consumer Access website. Every legitimate professional in California must hold a valid license from either the Department of Real Estate or the Department of Financial Protection and Innovation. Checking these credentials provides the peace of mind that you are working with an ethical, regulated partner.