What Happens If My Home Appraisal Is Low in San Jose? A 2026 Strategic Guide

In a market where the median sale price remains near $1.6 million, a low appraisal isn’t a dead end; it’s a strategic pivot point for a savvy buyer. You’ve likely spent weeks searching for the perfect home, only to feel your heart sink when the valuation comes in under your offer price. You’re probably wondering what happens if my home appraisal is low in san jose and whether your earnest money deposit is now at risk. It’s a stressful moment, but with 30-year fixed mortgage rates hovering around 6.5 percent, you have more leverage than you might think in this 2026 market reset.

We understand the anxiety of potentially overpaying or seeing a deal collapse over a loan-to-value ratio discrepancy. Our goal is to provide you with the clarity and peace of mind needed to move forward confidently. You’ll discover how to navigate the appraisal gap without losing your dream home or your hard-earned savings. We’ll walk you through successful price renegotiation strategies, specific mortgage restructuring options for Jumbo or Conventional loans, and how to challenge a valuation if the data doesn’t reflect the true local landscape.

Key Takeaways

- Understand how the Loan-to-Value ratio acts as the primary gatekeeper for your financing and why San Jose’s competitive dynamics often create valuation gaps.

- Learn how to leverage appraisal contingencies to protect your earnest money deposit, ensuring you don’t lose your capital if the deal doesn’t align with market value.

- Discover exactly what happens if my home appraisal is low in san jose and how to deploy strategic responses like the “Meet in the Middle” negotiation or a formal Reconsideration of Value.

- Identify the specific cash requirements needed to bridge a gap, as these costs often extend beyond a simple dollar-for-dollar price difference.

- See how integrated real estate and mortgage expertise can proactively prepare a “Value Package” to guide appraisers toward an accurate valuation from the start.

The San Jose Appraisal Gap: Why It Happens in 2026

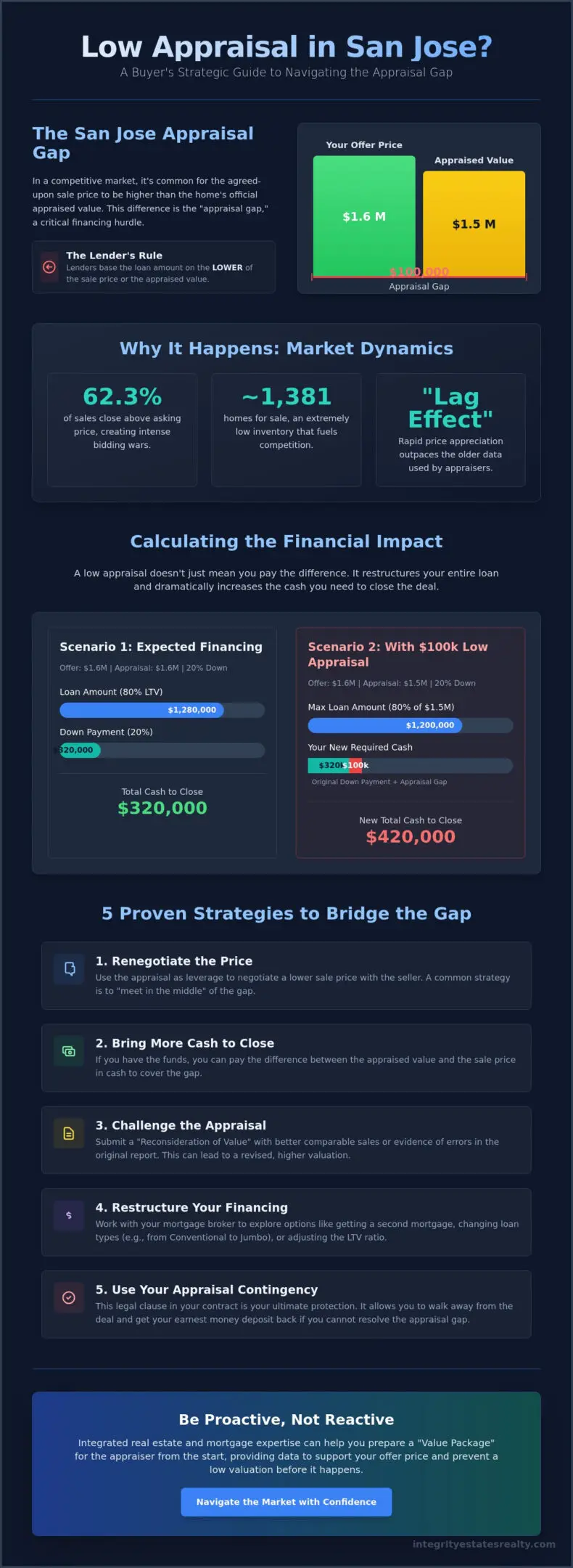

An appraisal gap occurs when the contract price agreed upon by a buyer and seller exceeds the fair market value determined by a licensed professional. In the high-stakes environment of Silicon Valley, this gap often surfaces during the final stages of a transaction, creating a moment of significant tension. Understanding what a home appraisal is helps clarify why this disconnect happens. It’s an objective assessment of value, but in a city like San Jose, objectivity often clashes with market velocity. When you find yourself asking what happens if my home appraisal is low in san jose, you’re essentially dealing with a divide between the price you’re willing to pay for a lifestyle and the value a lender is willing to secure as collateral.

San Jose’s market in 2026 is defined by intense, localized competition. With for-sale inventory holding at just 1,381 homes as of April, the scarcity of options naturally drives overbidding. Buyers in neighborhoods like Willow Glen or Almaden Valley often encounter the “Lag Effect.” This happens when the rapid appreciation of local properties outpaces the recorded data of previous sales. While you might see the value in a home’s proximity to tech campuses or its renovated kitchen, lenders prioritize conservative valuations. They care about the long-term stability of the asset, not the emotional excitement of a bidding war.

The Role of Comparable Sales in Santa Clara County

Appraisers in Santa Clara County typically select “comps” within a one-mile radius of the subject property. In a shifting market where mortgage rates recently settled near 6.56%, a sale from six months ago might not accurately capture current buyer sentiment. Time is a critical factor; if the most recent comparable sale was during a period of higher rates or lower inventory, the data may be skewed. Appraisers utilize the bracketed value technique by selecting comparable properties that sit both slightly above and slightly below the subject property’s characteristics to establish a logical price ceiling and floor.

Why 2026 Bidding Wars Create Valuation Friction

Bidding wars in 2026 are more calculated than the frenzied peaks of the past, yet they still drive prices significantly above list. In March 2026, 62.3% of San Jose sales closed over the asking price. In micro-markets like Berryessa or West San Jose, multiple offers remain a standard feature. While a stack of offers proves demand to a seller, it doesn’t always sway an appraiser who is looking for physical evidence of value. Knowing what happens if my home appraisal is low in san jose allows you to prepare for this psychological gap between market price and appraised value before it threatens your earnest money deposit.

Calculating the Financial Impact: LTV and Your Down Payment

When analyzing what happens if my home appraisal is low in san jose, the first thing to look at is your Loan-to-Value (LTV) ratio. This ratio is the “magic number” for lenders because it determines the level of risk they are assuming. Lenders follow a strict “lower of the two” rule; they will base your maximum loan amount on either the purchase price or the appraised value, whichever is lower. If you’ve bid $1.6 million on a property but the appraiser values it at $1.5 million, the bank ignores your high bid and calculates your financing based on that lower figure. This creates an immediate funding gap that must be addressed before the keys can change hands.

A shortfall in valuation doesn’t just mean you pay the difference. It fundamentally shifts your entire financial structure. Because the bank is lending against a smaller asset value, your original down payment percentage effectively shrinks. To maintain your original loan terms, you’re often required to bring significantly more cash to the closing table than the simple dollar-for-dollar difference of the gap. Understanding these nuances is why many buyers seek Mortgage Brokers in Santa Clara County who can navigate complex financing hurdles in real-time. If you find yourself facing a valuation hurdle, you can explore proven strategies to bridge the gap to keep your purchase on track.

The Math of a $100,000 Appraisal Shortfall

Consider a scenario where you’ve entered a contract for a $1.8 million home in San Jose with a 20% down payment of $360,000. If the appraisal comes back at $1.7 million, the bank will only lend 80% of that new, lower value, which is $1.36 million. Your total cash requirement jumps from $360,000 to $440,000 to keep the deal alive at the original price. An appraisal gap coverage clause is a contractual agreement where the buyer commits to paying a specific dollar amount above the appraised value if a shortfall occurs. This tool provides clarity for both parties, but it requires liquid reserves to be effective.

Mortgage Insurance (PMI) as a Strategic Tool

If you don’t have the extra $80,000 in liquid cash to cover a gap, taking on Private Mortgage Insurance (PMI) can be a brilliant strategic move. By shifting to a higher LTV loan, such as 90% or 95%, you can use your existing down payment funds to cover the price difference while still securing the property. While PMI adds a monthly cost, it’s often negligible compared to the long-term appreciation potential of a Silicon Valley asset. You might find that partnering with an expert advisor helps you weigh these technical debt structures against your personal financial goals.

Contingencies: Your Legal Shield in a Low Appraisal Scenario

The appraisal contingency is your most powerful tool for risk management in a high-velocity market. It functions as a legal escape hatch, ensuring that if the property’s valuation doesn’t meet the purchase price, you can withdraw from the contract without losing your Earnest Money Deposit (EMD). In San Jose, where a typical 3% deposit on a median-priced home can exceed $45,000, this protection is not just a formality; it’s a vital safeguard for your liquid capital. When you’re weighing what happens if my home appraisal is low in san jose, the presence of this clause dictates whether you’re negotiating from a position of strength or facing the potential loss of your deposit.

While many buyers feel pressured to submit “non-contingent” offers to remain competitive, this practice carries immense financial weight. Sellers often prioritize these offers because they remove the uncertainty of a valuation gap. However, regional data shows that market conditions vary significantly by zip code. For instance, the Gilroy Real Estate Market Trends: A Comprehensive 2026 Analysis indicates that while neighboring areas might allow for more flexibility, San Jose’s core neighborhoods remain rigid regarding deadlines and notice requirements. You must legally declare your intent to the seller within the specified contingency period, or you risk waiving your rights by default.

The “Partial Gap” Strategy in Competitive Bids

To win a bidding war without total exposure, many 2026 buyers utilize a “Partial Gap” strategy. Instead of a full waiver, you can write an offer that commits to covering a specific amount, such as the first $20,000 of a shortfall, while retaining the right to cancel if the gap exceeds that cap. Sellers often prefer these capped gaps over full contingencies because they provide a level of price certainty. We also recommend negotiating a “Right to Cure” for the seller, which allows them the first opportunity to lower their price to meet your maximum contribution before the deal dissolves.

What Happens If You Waived the Contingency?

If you signed a waiver and the appraisal comes in low, the legal reality in California is that the seller may be entitled to your EMD as liquidated damages if you fail to close. This is a stressful position, but it doesn’t always mean the deal is over. You can still find ways to Bounce Back From A Low Appraisal by exploring emergency financing pivots. This might include sourcing gift funds from family or securing secondary financing to cover the shortfall. Understanding what happens if my home appraisal is low in san jose when you’re non-contingent requires a methodical approach to restructuring your debt quickly to protect your initial investment.

5 Proven Strategies to Bridge the Gap and Close the Deal

Discovering what happens if my home appraisal is low in san jose is the first step toward saving your transaction. While a valuation shortfall feels like a crisis, it’s actually a common negotiation phase in Silicon Valley’s unique 2026 landscape. The seller wants to close, you want the home, and the lender wants to fund a viable asset. This shared interest creates the space for strategic problem-solving. By deploying one of these five proven methods, you can often bridge the financial divide without sacrificing your dream property.

- Strategy 1: Renegotiating the Sales Price. This “Meet in the Middle” approach is the most common resolution. If the seller knows that any subsequent buyer will likely face the same appraisal hurdle, they’re often willing to lower the price to keep the deal moving.

- Strategy 2: The Reconsideration of Value (ROV). This is a formal challenge to the appraiser’s findings. It’s not a simple complaint but a data-driven appeal that requires specific evidence of market value the appraiser may have overlooked.

- Strategy 3: Restructuring the Loan. By shifting from a 20% down payment to a 10% or 15% structure, you can reallocate your liquid cash to cover the appraisal gap while still meeting the lender’s LTV requirements.

- Strategy 4: Seller Credits and Creative Financing. If the seller won’t budge on price, they might offer a credit toward your closing costs. This frees up your personal funds to cover the valuation shortfall.

- Strategy 5: Ordering a Second Appraisal. If the first report contains significant factual errors, you can work with your lender to request a fresh valuation from a different professional, though this typically requires switching loan programs or lenders.

How to Successfully Challenge a Low Appraisal

A successful “CMA Defense” involves providing the appraiser with superior comparable sales they might have missed, particularly those that closed in the last 30 days. We look for factual errors in the initial report, such as incorrect square footage, missed room counts, or overlooked upgrades like high-end ADUs or solar installations. In 2026, a formal ROV submission must include a minimum of three comparable sales that weren’t utilized in the initial report, accompanied by a specific narrative justifying their relevance. This methodical approach ensures the lender sees the true market narrative rather than just a conservative data set.

The Loan Restructure: A Mortgage Broker’s Secret Weapon

Your lender choice matters immensely when you’re asking what happens if my home appraisal is low in san jose. A flexible brokerage can pivot your loan program mid-escrow to accommodate a lower valuation. While San Jose often requires Jumbo financing, understanding FHA Home Loans in Gilroy, CA: Your 2026 Guide to Affordable Home Financing provides insight into how different loan programs handle appraisal flexibility and lower down payment requirements. If you’re facing a valuation hurdle, connect with Integrity Estates to explore a custom financing pivot that protects your earnest money and secures your home.

The Integrity Estates Advantage: Real Estate Meets Mortgage Expertise

Most real estate firms treat the valuation process as an external variable they can’t control. At Integrity Estates, we view the appraisal as a critical milestone that requires proactive management. When you partner with a firm that handles both the property search and the financing, the question of what happens if my home appraisal is low in san jose becomes a technical challenge we solve rather than a crisis that ends your escrow. Our dual-licensed status as both a real estate agency and a mortgage brokerage allows us to pivot instantly, restructuring Jumbo or Conventional loans without the delays typical of third-party lenders.

Maria Elena “Nena” Arriaga brings over 20 years of local experience to every transaction, providing a level of regional insight that a standard data report simply cannot replicate. We don’t just wait for the appraiser to call; we prepare a comprehensive “Value Package” for them before they even step onto the property. This package includes a curated list of upgrades, hyper-local neighborhood highlights, and the most recent comparable sales that justify the contract price. This proactive approach often prevents a low valuation before it occurs, protecting your equity and your peace of mind.

Consider a recent case in West San Jose where a client faced a $100,000 appraisal shortfall on a $1.7 million purchase. While a traditional agent might have simply asked the buyer for more cash, Nena utilized her mortgage expertise to restructure the buyer’s Jumbo Loan. By adjusting the loan-to-value parameters and reallocating funds, she saved the deal and protected the client’s earnest money deposit. Our team provides the steady guidance needed to understand exactly what happens if my home appraisal is low in san jose, turning a stressful shortfall into a successful closing.

Pre-Appraisal Preparation for Sellers

If you’re on the selling side, justifying your asking price to a bank’s representative is essential for a smooth exit. We help you document every improvement, from high-efficiency HVAC systems to custom kitchen cabinetry, ensuring the appraiser sees the full value of your investment. For those looking to maximize their return in the current market, our Sell My Home in Gilroy: The 2026 Strategic Guide to Maximum Equity offers deeper insights into preparing your property for the highest possible valuation.

Your Next Steps: Don’t Panic, Pivot

The first 24 hours after receiving a low appraisal are the most critical. You need an immediate analysis of your contract’s contingency dates and a clear look at your mortgage restructuring options. Don’t let a conservative valuation derail your long-term goals or cost you your deposit. Schedule a strategy session with our integrated real estate and mortgage team to find your path forward. Contact Integrity Estates Realty for a Professional Consultation and let us guide you through the complexities of the San Jose market with confidence.

Turning Valuation Challenges into Closing Success

A low appraisal in the San Jose market doesn’t have to signal the end of your homeownership journey. By understanding the technical nuances of your Loan-to-Value ratio and leveraging strategic contingencies, you can protect your earnest money while pursuing the property you love. Success in this competitive landscape depends on your ability to pivot quickly, whether through a formal Reconsideration of Value or a creative loan restructure. Understanding exactly what happens if my home appraisal is low in san jose allows you to move from a state of anxiety to a position of informed action.

Integrity Estates Realty provides the sophisticated guidance required for these high-stakes moments. As an independently owned firm led by Maria Elena “Nena” Arriaga, we bring over 20 years of Santa Clara County expertise to your side. Our dual-licensed Real Estate and Mortgage Brokerage model ensures that your representation and financing work in perfect harmony. Navigate your San Jose home purchase with the experts at Integrity Estates Realty and secure your future in Silicon Valley. You have the tools and the right team to make this move a reality.

Frequently Asked Questions

Can I cancel my contract if the appraisal is lower than the purchase price in San Jose?

Yes, you can cancel the contract and retain your earnest money deposit if your agreement includes an appraisal contingency. This clause acts as a safety net, allowing you to withdraw if the bank’s valuation doesn’t match the purchase price. However, if you waived this contingency to remain competitive in a bidding war, canceling the deal would likely result in the forfeiture of your deposit to the seller.

How much extra cash do I need if my appraisal is $50,000 low?

The amount of cash required often exceeds the $50,000 shortfall because of how lenders calculate the Loan-to-Value (LTV) ratio. Since the bank only lends a percentage of the appraised value, a lower valuation reduces your total loan amount. You’ll need to cover both the $50,000 price gap and the difference in the financed amount to keep your original down payment structure intact.

Will a low appraisal affect my interest rate or loan terms?

A low appraisal can trigger changes to your loan terms if it pushes your LTV ratio into a higher risk category. For example, if your ratio moves from 80% to 85%, you might be required to pay Private Mortgage Insurance (PMI) or accept a slightly higher interest rate. Understanding what happens if my home appraisal is low in san jose is crucial because these shifts can alter your monthly mortgage payment significantly.

Who pays for a second appraisal if I want to challenge the first one?

The buyer is typically responsible for the cost of a second appraisal. Lenders generally don’t cover this expense and will only order a second report under specific circumstances, such as a change in the loan program or evidence of significant errors in the first report. It’s often more efficient to attempt a Reconsideration of Value before paying for an entirely new assessment.

How long does the Reconsideration of Value (ROV) process take in Santa Clara County?

The ROV process usually takes between 5 and 10 business days in Santa Clara County. This timeline accounts for the time needed to gather new comparable sales, the lender’s internal review, and the appraiser’s response. In 2026, new California regulations require appraisers to complete specific training on valuation bias, which has standardized the review process but hasn’t necessarily shortened the turnaround time.

Is a low appraisal the same as a bad home inspection?

No, these are entirely different evaluations. A home inspection focuses on the physical condition, safety, and mechanical systems of the property. An appraisal is a financial assessment used by the lender to determine the property’s value as collateral. A home in pristine physical condition can still receive a low appraisal if local comparable sales from the last few months don’t support the contract price.

Does a low appraisal mean I am overpaying for the house?

Not necessarily. Appraisals often rely on historical data that may lag behind the real-time demand of the San Jose market. If you’re buying in a neighborhood with rapidly increasing activity, the appraiser’s “comps” might not yet reflect the current lifestyle value or the scarcity of inventory. It’s a reflection of conservative bank guidelines rather than a definitive statement on the home’s future potential.

Can the seller refuse to lower the price after a low appraisal?

Yes, the seller is under no legal obligation to reduce their price to match the appraised value. In a market where 62.3% of homes recently sold over the list price, some sellers may choose to wait for a buyer with more liquid cash. When you’re navigating what happens if my home appraisal is low in san jose, this refusal often leads to a negotiation where both parties “meet in the middle” to save the transaction.