When to Refinance Your Mortgage in San Jose: A 2026 Strategic Guide

In the high-stakes environment of Silicon Valley, a simple dip in interest rates is rarely enough to tell you when to refinance mortgage san jose. With median home values holding steady at $1.45 million, even a fractional change in your rate can translate into a massive difference in your long-term wealth. You’re likely managing a complex financial portfolio where your primary residence is just one piece of the puzzle, and the pressure to optimize that debt while balancing RSU vesting schedules can feel overwhelming.

We understand that a standard mortgage calculator doesn’t account for the nuances of your tech-heavy income or the specific jumbo loan limits in Santa Clara County. This guide promises to cut through the noise, offering you a sophisticated “Go/No-Go” framework to determine if the 2026 market conditions align with your personal goals. You’ll discover how to evaluate the ROI of a refinance by looking at your total compensation, including bonuses and equity, rather than just your base salary. We will walk you through the strategic triggers for 15-year versus 30-year terms and show you exactly how to lower your monthly interest on those significant Silicon Valley balances.

Key Takeaways

- Understand the “San Jose Multiplier” and why even a modest rate reduction on high-balance Silicon Valley loans can yield substantial long-term savings.

- Identify the specific credit score thresholds and financial triggers that determine exactly when to refinance mortgage san jose to maximize your return on investment.

- Learn how to strategically align your application with RSU vesting schedules and annual bonuses to strengthen your qualification for competitive Jumbo loan rates.

- Compare the long-term benefits of a traditional refinance against a mortgage recast to find the most cost-effective path for your specific financial landscape.

- Discover how a holistic approach to your property equity can transform your mortgage from a monthly debt into a sophisticated wealth-building tool.

The Financial Case for Refinancing in the San Jose Market

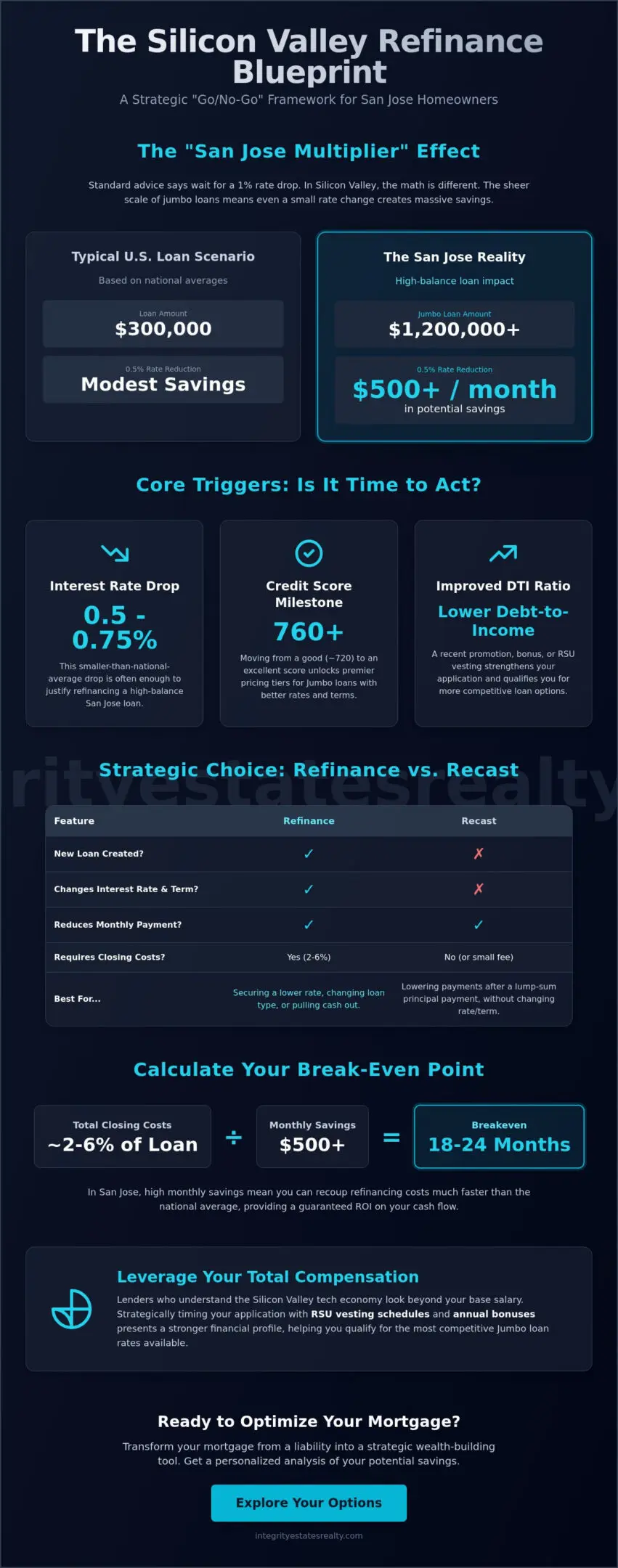

National mortgage advice often falls short when applied to the unique economic climate of Silicon Valley. Standard financial wisdom suggests waiting for a full 1% drop in interest rates before considering a change, but this ignores the “San Jose Multiplier.” On a typical $300,000 mortgage, a 0.5% rate reduction might save a few hundred dollars monthly. In San Jose, where a $1.2 million loan is the baseline for many families, that same 0.5% shift can save over $500 every single month. When you’re deciding when to refinance mortgage san jose, the sheer scale of your loan balance makes even small rate adjustments highly profitable.

With the average home value in San Jose reaching $1,452,609 as of April 2026, the rapid accumulation of equity creates unique windows of opportunity. This growth allows homeowners to transition from high-interest Jumbo loans into more favorable terms or potentially eliminate private mortgage insurance much faster than the national average. Moving from being “house poor” to “equity rich” isn’t just a psychological relief; it’s a strategic financial pivot that frees up capital for other high-yield investments or lifestyle goals.

Amortization Realities for Jumbo Loans

Interest costs are heavily front-loaded on high-balance loans. For a San Jose resident with a 30-year jumbo refinance rate hovering around 6.77%, the amount of capital directed toward interest in the first five years is staggering. Trimming just five years off your term or securing a lower rate early in the loan lifecycle can save hundreds of thousands of dollars in total interest. It’s about more than just the monthly payment; it’s about the total cost of ownership. If you’re unsure where you currently stand on your amortization schedule, consulting with mortgage brokers in Santa Clara County can provide a personalized look at your potential savings.

Calculating Your Break-Even Point in California

Before committing to a new loan, you must identify your break-even point. This is the specific month where your cumulative monthly savings finally offset the closing costs of the transaction. While What is refinancing? covers the broad concept of replacing debt, the local calculation in Santa Clara County is often more aggressive. Refinancing costs in California typically range from 2% to 6% of the loan amount. However, because San Jose loan balances are so high, the monthly savings are often large enough to recoup these costs in as little as 18 to 24 months. In a market where tech stocks and RSU values fluctuate, locking in a lower fixed monthly debt provides a rare form of guaranteed ROI. It’s a calculated move to protect your cash flow from the inherent volatility of the broader Silicon Valley economy.

Core Triggers: When Does Refinancing Make Sense?

Identifying the exact moment to act requires looking beyond national headlines. While many markets wait for a full 1% drop in rates, the high balances in Santa Clara County mean a 0.5% to 0.75% reduction often justifies the move. This sensitivity to smaller fluctuations is a primary factor in when to refinance mortgage san jose. If your loan balance exceeds $1 million, even a minor improvement in market conditions can result in thousands of dollars in annual savings. It’s a game of precision where timing is everything.

Credit score milestones represent another vital trigger. Lenders for Jumbo loans are particularly sensitive to specific credit tiers. Moving from a 720 to a 760+ score can shift you into a premier pricing bracket. This transition often unlocks lower interest rates and more flexible terms that aren’t available to those in lower tiers. It’s a simple change that yields significant long-term rewards.

Your debt-to-income (DTI) ratio also plays a decisive role in your eligibility. If you’ve recently received a major promotion or a significant increase in your compensation package, your improved DTI could qualify you for better terms. Leveraging Silicon Valley income like RSUs and bonuses allows you to present a more robust financial profile to underwriters who understand the local tech economy. They see the value in your total compensation, not just your base salary.

Switching from Adjustable to Fixed Rates

Many San Jose homeowners opted for ARMs when initial rates were lower, but the landscape has shifted. In a volatile 2026 economy, the risk of an upward rate reset can create unnecessary financial stress. Families in established neighborhoods like Almaden Valley often choose to lock in a fixed rate before their adjustable term expires. Timing this switch before the first rate adjustment cap is reached can prevent your monthly payment from spiking unexpectedly. It’s a strategy rooted in long-term stability and peace of mind.

Shortening the Term for Faster Payoff

If your cash flow allows, moving from a 30-year to a 15-year mortgage is a powerful way to build equity rapidly. As of June 2026, 15-year fixed refinance rates average 5.72%, which is a full percentage point lower than most 30-year options. While the monthly obligation increases, the trade-off is a massive reduction in total interest paid. For high-income earners, this is often the most direct path to total homeownership. Reviewing your current loan terms against these milestones is the first step toward a more secure financial future. You might find it helpful to explore customized refinancing options that align with your current career trajectory.

Refinancing vs. Recasting: Which is Better for You?

Deciding when to refinance mortgage san jose often involves a choice between replacing your entire loan or simply adjusting the one you have. For homeowners who secured sub-4% rates years ago, a traditional refinance might not make financial sense in the 2026 market. This is where a mortgage recast becomes a sophisticated alternative. While a refinance mortgage Gilroy homeowners might pursue involves a complete new loan with a new rate, a recast allows you to keep your existing interest rate while lowering your monthly obligation.

The Power of the Mortgage Recast

A mortgage recast is often the secret weapon for Silicon Valley professionals. Instead of starting over with a new interest rate and term, you make a significant lump-sum payment toward your principal balance. Your lender then re-amortizes the remaining balance over your original timeline. This process doesn’t change your rate; it simply shrinks your monthly payment based on the smaller debt. It is a perfect strategy for those who have recently liquidated RSUs or received a substantial annual performance bonus. Unlike a refinance, which can cost thousands in closing fees, a recast typically requires only a small administrative fee. It is a highly efficient way to improve your monthly cash flow without sacrificing a historically low rate.

Traditional Refinance Pros and Cons

There are still many scenarios where a traditional refinance is the superior choice. If your goal is to access your home’s equity for a major renovation or to consolidate high-interest debt, a cash-out refinance is necessary. In the 2026 interest environment, a 15-year fixed rate at approximately 5.72% offers a compelling path for those looking to accelerate their wealth building. The primary drawback remains the closing costs, which often range from 2% to 6% of the loan amount. For a high-balance San Jose mortgage, this can be a significant upfront investment that requires a longer stay in the home to recoup.

Consider a professional in Willow Glen with a $1.2 million balance at a 7.5% interest rate from a previous peak. If they can refinance into a 30-year term at the June 2026 average of 6.76%, the monthly savings would be substantial. However, if that same professional already has a 3.5% rate, they should skip the refinance and use their bonus to recast instead. The right choice depends entirely on your current rate and your immediate need for liquidity versus long-term interest savings. We can help you model these scenarios to ensure your decision aligns with your broader financial narrative.

Leveraging Silicon Valley Income: RSUs and Bonuses

The financial rhythm of San Jose is often dictated by the quarterly vesting of Restricted Stock Units (RSUs) and annual performance bonuses. For many tech professionals, these liquid events represent the most opportune times to evaluate when to refinance mortgage san jose. While standard borrowers rely strictly on monthly cash flow, Silicon Valley homeowners can use these windfalls to significantly alter their loan trajectory. Timing an application to coincide with high-income months allows you to satisfy the stringent debt-to-income requirements for “Super Jumbo” loans. These high-balance products often offer more competitive pricing for well-capitalized borrowers who can prove a consistent history of total compensation.

We often recommend the “Windfall Rule” to our clients. This strategy involves committing a predetermined percentage of every major bonus or vest toward a principal reduction during a refinance. Because loan balances in Santa Clara County are frequently above the 2026 conforming limit of $1,249,125, even a 5% reduction in principal can move the needle on your interest rate tier. It’s a method of turning corporate success into tangible home equity, providing a sense of permanence in an often volatile industry.

Turning Stock Vesting Into Home Equity

The “Equity Swap” is a strategic move where you trade volatile tech stock for the stability of debt-free real estate equity. Rather than letting vested shares sit in a brokerage account subject to market swings, many homeowners sell a portion to pay down their principal during a refinance. This reduction can help you cross the 20% equity threshold, potentially eliminating private mortgage insurance. It is essential to remember that California’s mandatory supplemental withholding rate on RSU vests is 10.23% for 2026. You’ll need to work with a partner who knows how to document this income correctly for underwriters. They must look past your base salary to your “Total Compensation” to ensure you receive the most favorable terms available.

Maximizing “Bonus Season” for Refinancing

The first quarter of the year is often the most active period for refinancing in Santa Clara County. This “Bonus Season” provides the necessary liquidity to cover closing costs without dipping into your emergency savings. You might also choose to use these funds to purchase discount points, effectively buying a lower interest rate for the life of the loan. Interest-saving velocity is the rate at which early payments or strategic refinancing reduce the total lifespan and cost of your mortgage. By front-loading these costs during a high-income month, you maximize your long-term ROI and accelerate your path to total ownership.

If you are expecting a significant vest or bonus soon, it’s the perfect time to prepare your documentation. We invite you to connect with our team for a comprehensive refinance strategy that integrates your equity compensation into your long-term homeownership goals.

Partnering with Integrity Estates Realty for Your Refinance

Deciding when to refinance mortgage san jose is a high-stakes choice that requires more than just a digital calculator. It demands a partner who understands the intricate relationship between Silicon Valley property values and complex financing structures. At Integrity Estates Realty, we provide a holistic perspective that bridges the gap between traditional real estate brokerage and expert mortgage origination. We don’t view your mortgage as an isolated debt; we see it as a pivotal component of your broader financial narrative. Our dual expertise allows us to analyze how a new loan impacts your total equity and long-term wealth preservation.

Our commitment to ethical conduct is the cornerstone of every relationship we build. We operate with a simple, transparent rule: we only recommend a refinance if the mathematical reality clearly benefits your bottom line. If the break-even point is too distant or if your current rate remains your best option, we will tell you directly. This reliability is why San Jose homeowners trust us to act as their steadfast guides through the volatility of the 2026 market. We take immense pride in being regional experts who understand the nuances of Santa Clara and Monterey County, ensuring your strategy is rooted in local market truths rather than generic national trends.

Comprehensive Mortgage and Equity Reviews

We treat your home as a primary asset within a larger portfolio. During a comprehensive review, we look at your current equity levels and career trajectory to determine the most efficient path forward. Sometimes, the best use of your capital isn’t a mortgage payoff. Depending on your goals, we might explore whether you are better served by investing in commercial real estate to diversify your holdings. This high-minded approach ensures that every transaction is purposeful and aligned with your lifestyle curation goals. It is the “Integrity” difference: prioritizing your peace of mind over a quick transaction.

Your Personalized San Jose Roadmap

Every homeowner’s journey is unique, especially in a market dominated by high-balance requirements. We create customized roadmaps for FHA, VA, and Jumbo loan holders that account for the specific challenges of the Silicon Valley landscape. Because we maintain relationships with a wide network of wholesale lenders, we can often secure competitive rates and terms that aren’t available through traditional retail banks. We handle the heavy lifting of the application and processing, allowing you to focus on your career and family while we optimize your debt.

Your equity is a powerful tool, and 2026 is the year to ensure it is working as hard as you are. We invite you to take the next step in your financial journey with a partner who is as invested in your future as you are. Schedule your 2026 Mortgage Consultation with Integrity Estates Realty today and discover the clarity that comes from expert, local guidance.

Your Path to Long-Term Wealth in San Jose

Navigating the 2026 mortgage landscape requires a strategy as sophisticated as the Silicon Valley economy itself. We’ve explored how the high loan balances in Santa Clara County amplify the impact of every rate shift and why your RSU vesting schedule is a critical component of your timing. Whether you choose a traditional refinance to capture current market lows or a strategic recast to lower your monthly obligation, the goal remains the same: transforming your home equity into a stable foundation for your future.

Deciding exactly when to refinance mortgage san jose shouldn’t be a source of stress. With over 20 years of local expertise, Integrity Estates Realty provides the integrated real estate and mortgage services you need to make an informed choice. As an independently owned brokerage led by Maria Elena “Nena” Arriaga, we’re dedicated to providing the transparent, ethical guidance that ensures your next move is your best move.

Analyze Your Refinance Strategy with Our San Jose Experts and take control of your financial narrative today. You’ve worked hard for your home; it’s time to make sure your mortgage is working just as hard for you.

Frequently Asked Questions

Does San Jose have specific laws regarding mortgage prepayment penalties?

California law generally protects homeowners from excessive prepayment penalties on residential properties with one to four units. Under Civil Code 2954.9, most borrowers have the right to pay down their principal early without heavy fees after the first few years of the loan. However, it’s vital to review your specific note, especially for non-conforming Jumbo loans or investment properties, to ensure you aren’t penalized for a strategic early exit.

How much interest can I save by refinancing a $1.2 million Jumbo loan in San Jose?

The savings on a high-balance loan are substantial due to the sheer scale of the principal. Trimming just 0.5% from a $1.2 million balance can reduce your annual interest expense by approximately $6,000. Over the life of the loan, this strategic move can preserve hundreds of thousands of dollars in personal wealth that would otherwise go toward bank interest. This is the primary driver for many when deciding when to refinance mortgage san jose.

Is it better to refinance or pay off my mortgage early with RSUs?

This decision depends on your current interest rate and your broader investment goals. If your mortgage rate is lower than the expected return on your diversified investments, refinancing to a more favorable term might be wiser than a total payoff. Using RSUs to pay down principal can lower your debt, but keeping some liquidity often provides a more balanced financial roadmap in the volatile Silicon Valley tech sector.

What is a mortgage recast and do San Jose lenders typically offer it?

A mortgage recast involves making a large principal payment and asking your lender to re-calculate your monthly payments based on the new, lower balance. Unlike a refinance, your interest rate and term remain the same. Most major lenders in the San Jose area offer this service for a small administrative fee, making it an excellent tool for those with significant annual bonuses or stock vests who want to lower their monthly obligation.

Can I use my RSU income to qualify for a 15-year refinance term?

Yes, lenders in Silicon Valley are increasingly adept at factoring equity compensation into your debt-to-income ratio. To qualify for the accelerated 15-year term, you’ll need to provide a consistent history of vesting and proof that the income is likely to continue. Documenting your total compensation correctly is essential to securing the most competitive rates available in Santa Clara County for high-income professionals.

Should I refinance if I plan to sell my San Jose home in less than 3 years?

Refinancing is rarely beneficial if you plan to move within a short window. The process involves closing costs that typically range from 2% to 6% of the loan amount. If you sell your home before you reach the break-even point where monthly savings offset these costs, you’ll likely lose money on the transaction. We always recommend a thorough cost-benefit analysis if you anticipate a move in the near future.

How do closing costs in Santa Clara County compare to the national average?

Closing costs in Santa Clara County are often higher in absolute dollars because they are calculated as a percentage of much larger loan balances. While the national average might seem lower, the sophisticated nature of San Jose’s Jumbo loans and local title fees requires a larger upfront investment. However, the high monthly savings potential in our market often leads to a faster break-even period than in lower-cost regions.

What is the “Magic Number” for interest rate drops to justify a refinance in 2026?

In the 2026 market, the old “1% Rule” is outdated for the San Jose area. Because of our massive loan balances, a drop of just 0.5% to 0.75% is often enough to justify a change. The key is to calculate your specific break-even point. If you can recoup your costs within 24 months through lower monthly payments, the move is usually a sound financial decision for your long-term wealth.