How to Get Pre-Approved for a Mortgage in San Jose: A 2026 Buyer’s Roadmap

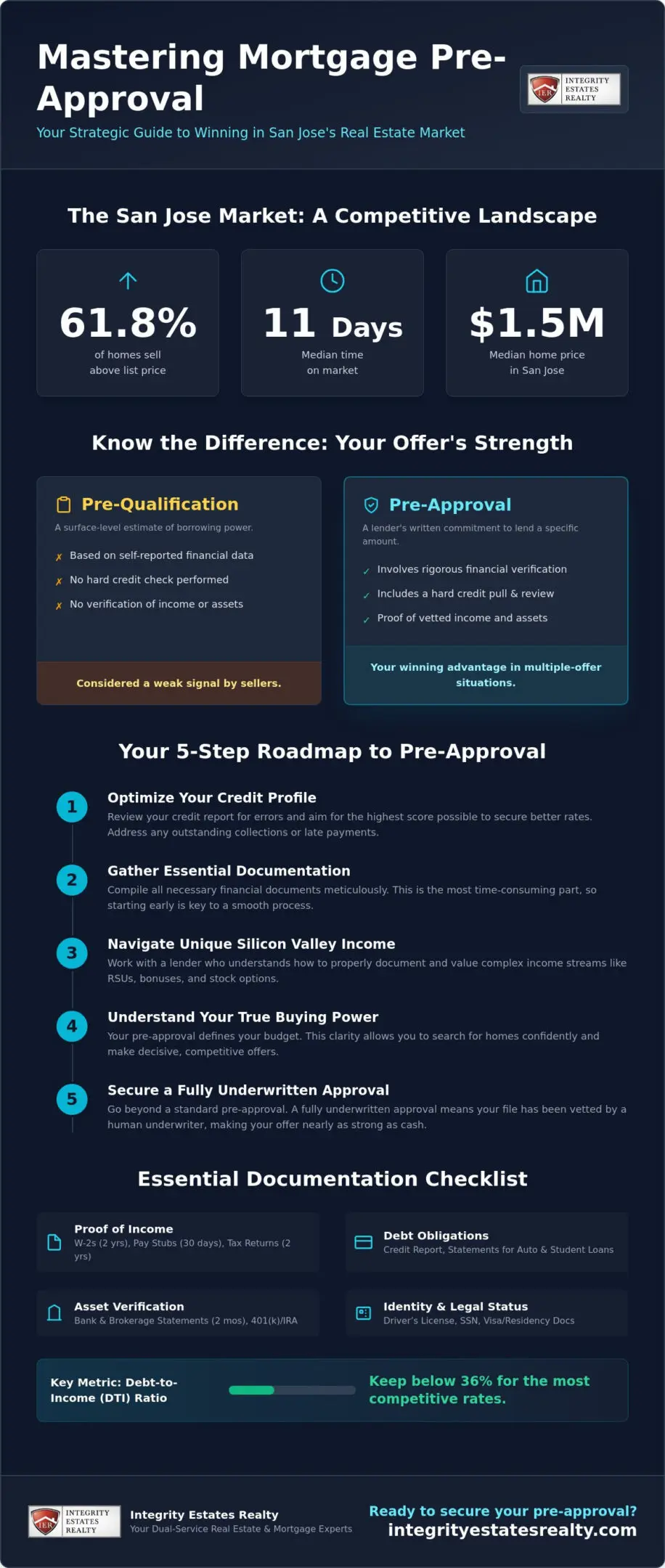

With 61.8% of homes in San Jose selling above their list price and a median time on market of just 11 days, your offer must be flawless before it even hits the seller’s desk. In the fast-paced Silicon Valley environment, a standard letter isn’t enough to win. Learning how to get pre-approved for a mortgage in san jose is the essential first step to becoming a serious contender in this market. It’s about more than just a credit score. It’s about translating complex RSU packages, bonuses, and high-balance loan requirements into a financial profile that commands respect from sellers and agents alike.

We understand that managing the complexities of the Santa Clara County real estate market can feel like a high-stakes puzzle, particularly when your income doesn’t fit into a traditional box. You deserve a clear path that replaces anxiety with a sense of certainty and professional poise. This guide provides a comprehensive roadmap to mastering your pre-approval, ensuring you understand your true buying power and the nuances of the 2026 mortgage market. We’ll explore the specific documentation needed for tech professionals, the strategy behind fully underwritten approvals, and how to position yourself as the most reliable buyer in the room.

Key Takeaways

- Discover why a fully underwritten pre-approval is the essential strategic asset you need to compete in a market where homes often sell in under two weeks.

- Identify the specific documentation required to verify complex Silicon Valley income streams, including the last two years of tax returns and current asset statements.

- Master the nuances of how to get pre-approved for a mortgage in san jose when navigating high-balance jumbo loans and restricted stock unit (RSU) valuations.

- Follow our five-step roadmap to optimize your credit profile and establish a clear understanding of your true buying power before entering negotiations.

- Learn the unique advantages of partnering with a dual-service brokerage that offers both local real estate expertise and specialized mortgage processing.

Why Mortgage Pre-Approval is Your Competitive Edge in San Jose

In San Jose, where the median home price hovers around $1.5 million, a simple offer isn’t a strategy; it’s a gamble. Mastering how to get pre-approved for a mortgage in san jose is your first step toward securing a home in this competitive landscape. Sellers in Santa Clara County don’t just look for a high price. They look for the path of least resistance. A mortgage pre-approval acts as a lender’s written commitment to provide a specific loan amount based on a deep dive into your financial history. Understanding what mortgage pre-approval means is vital because it transforms you from a window shopper into a verified buyer. It signals to listing agents that you have the financial integrity to close the deal, even in a market where interest rates fluctuate between 6.49% and 6.6% as they have in mid-2026.

Pre-Approval vs. Pre-Qualification: Know the Difference

Many buyers confuse these terms, which is a mistake that can cost you your dream home in Almaden Valley. Pre-qualification is a surface-level estimate. It relies on self-reported data and doesn’t involve a hard credit check. In contrast, knowing how to get pre-approved for a mortgage in san jose involves a rigorous verification of your W-2s, tax returns, and asset statements. Sellers view a pre-approval as a cash-equivalent safety net. It proves a professional underwriter has already vetted your file, reducing the risk of a deal falling through during the escrow period.

Winning Multiple-Offer Wars in Silicon Valley

With 61.8% of San Jose homes selling above list price in 2026, you’re likely to face competition. A strong pre-approval letter allows your agent to negotiate shorter financing contingencies, sometimes as short as 7 to 10 days. This speed is a massive psychological advantage. When a seller in Willow Glen sees a pre-approval from a local expert like Integrity Estates Realty, they feel a sense of security. They know the lender understands the nuances of Santa Clara County property values and the local tech-driven economy. By positioning yourself as a sure thing, you often win against higher offers that have shaky or non-local financing.

The 2026 market demands agility. With active listings up 17.6% year-over-year as of April, you have more choices, but the best properties still disappear in an average of 11 days. Early financing isn’t just about the letter. It’s about locking in your buying power before market shifts occur. Having your documentation ready allows you to act the moment a listing hits the market, giving you a head start that unprepared buyers simply cannot match. This preparation provides peace of mind, replacing the frantic energy of a last-minute scramble with a composed, methodical approach to your home search.

Essential Documentation for a Santa Clara County Mortgage

Collecting the right paperwork is often the most time-consuming part of the journey. In a market where the median home price was $1.5 million in early 2026, lenders require absolute precision to minimize risk. Understanding how to get pre-approved for a mortgage in san jose starts with building a meticulous financial dossier that proves your ability to handle a high-balance loan. This isn’t just about showing you have the money; it’s about proving where it came from and how stable it is.

- Proof of Income: Expect to provide your two most recent W-2 forms and pay stubs covering the last 30 days. Lenders also require full federal tax returns from the past two years to verify income consistency.

- Asset Verification: You’ll need two months of complete statements for all checking, savings, and brokerage accounts. Include your 401(k) or IRA statements to demonstrate you have the necessary reserves for a jumbo loan.

- Debt Obligations: Lenders pull your credit report to see credit cards, student loans, and auto loans. They use this to calculate your Debt-to-Income (DTI) ratio, which ideally should be below 36% for the most competitive rates.

- Identity and Legal Status: A valid driver’s license and social security number are standard requirements. If you’re a non-citizen, you’ll need to provide documentation regarding your residency or visa status.

The ‘Paper Trail’ for Down Payments

Silicon Valley’s high entry costs often mean buyers utilize gift funds from family. If you’re receiving help, you’ll need a signed gift letter and a clear audit trail of the transfer. Lenders look for seasoned funds. This means money should ideally be in your account for at least 60 days. If you’re moving large sums between accounts, keep every receipt. Sudden, unexplained deposits can trigger red flags during underwriting and delay your approval. If you want to ensure your documentation is airtight, seeking professional mortgage guidance can save you weeks of back-and-forth with underwriters.

Special Requirements for Self-Employed Buyers

For the many entrepreneurs and consultants in Santa Clara County, the process is more detailed. You’ll likely need a year-to-date Profit and Loss (P&L) statement and a balance sheet. Business tax returns and K-1 forms are essential to prove the stability of your income. Because self-employed earnings can fluctuate, providing a clear narrative of your business’s health is key to how to get pre-approved for a mortgage in san jose. Lenders want to see that your business is not just surviving, but thriving enough to support a long-term mortgage commitment.

Navigating San Jose’s Unique Financial Landscape: RSUs and Jumbo Loans

San Jose’s economy is powered by innovation, but that same innovation often complicates a standard mortgage application. If your income includes Restricted Stock Units (RSUs) or performance-based bonuses, you’ll find that generic online lenders often struggle to calculate your true qualifying income. Learning how to get pre-approved for a mortgage in san jose means finding a partner who understands that a base salary is only one part of your financial story. In 2026, lenders specialize in translating these complex tech packages into a credible profile that underwriters can approve with confidence. It’s about ensuring your total compensation is recognized, not just your monthly paycheck.

RSUs and Variable Income: Making it Count

Stock-based compensation is a cornerstone of Silicon Valley wealth, yet it requires a specific approach during the pre-approval process. Most lenders adhere to a two-year history rule, looking for consistent vesting patterns to ensure the income is stable and likely to continue. To make this income count toward your loan amount, you’ll need to provide your official vesting schedules and grant letters. These documents act as evidence of your future earning potential. A local broker who speaks the language of the tech sector knows how to present this data to an underwriter. This expertise ensures your RSUs are treated as a reliable asset rather than a variable risk, which is crucial for maintaining a healthy debt-to-income (DTI) ratio in a high-cost area.

Jumbo Loan Requirements in San Jose

With the median sold price in San Jose reaching approximately $1.5 million in early 2026, many buyers naturally move beyond standard loan limits. In Santa Clara County, the high-balance conforming limit for a single-family home is $1,249,125. Any loan amount exceeding this figure is classified as a jumbo loan. These high-value transactions come with stricter requirements, often demanding higher credit scores and significant cash reserves. It’s common for lenders to require liquid assets that can cover 6 to 12 months of mortgage payments as a safety net.

Navigating these hurdles is a standard part of how to get pre-approved for a mortgage in san jose. While some programs may offer jumbo loans with down payments as low as 5%, the most favorable interest rates often require a larger equity stake and a DTI below 36%. For a more technical breakdown of these limits and how they impact your buying power, explore our comprehensive Jumbo loan santa clara county guide. By aligning your financial strategy with local market realities, you ensure that your pre-approval letter is a sophisticated reflection of your actual wealth, giving you the leverage needed to secure a home in premium neighborhoods.

The 5-Step San Jose Mortgage Pre-Approval Process

Securing a home in Silicon Valley requires a methodical approach that generic online platforms often overlook. Understanding how to get pre-approved for a mortgage in san jose involves a five-step journey designed to build a bulletproof financial profile. This isn’t a “click and receive” experience. It’s a professional collaboration that ensures your financing is as resilient as your ambition. By following this structured roadmap, you move from uncertainty to a position of absolute market readiness.

- Step 1: Initial Consultation and Goal Setting. We begin by aligning your financial capabilities with your lifestyle aspirations. This phase defines your comfortable price range and identifies any potential hurdles early on.

- Step 2: Comprehensive Credit Review. We perform a deep dive into your credit history to ensure your score is optimized for the best possible interest rates.

- Step 3: Document Submission. You’ll provide the financial “paper trail” we detailed earlier. A professional underwriter then reviews this data to verify every dollar of income and assets.

- Step 4: Loan Program Selection. We evaluate whether an FHA, VA, Conventional, or Jumbo loan best serves your long-term wealth strategy.

- Step 5: Issuance of the Strategic Pre-Approval Letter. You receive a formal document that signals your readiness to sellers, giving you the leverage to win.

Credit Score Optimization for Better Rates

Even a minor error on a credit report can impact your interest rate significantly. When you’re looking at how to get pre-approved for a mortgage in san jose, we focus on identifying and disputing these inaccuracies before the final pull. High credit utilization can also shrink your buying power. We advise keeping balances low and avoiding new credit inquiries, such as car loans or new credit cards, during this sensitive phase. A few points on your score can translate into thousands of dollars saved over the life of your loan.

Choosing the Right Loan Program

Every buyer’s path is unique. For those looking at more accessible entry points in the region, exploring FHA home loans in Gilroy can be a smart move if you have a lower down payment. Veterans in the San Jose area can leverage specialized VA loan benefits that often offer competitive terms without a traditional down payment. For most Silicon Valley transactions, the choice between conventional and jumbo financing depends on the current $1,249,125 high-balance limit. We help you find the “sweet spot” where your monthly commitment matches your personal narrative of homeownership. Ready to secure your place in the market? Start your pre-approval with our local experts today to ensure your offer stands out.

Partnering with Integrity Estates Realty for Your San Jose Home

Choosing the right guide is as important as choosing the right property. When you’re determining how to get pre-approved for a mortgage in san jose, you’re not just looking for a letter; you’re looking for a partnership that spans the entire transaction. Integrity Estates Realty offers a unique dual-service model, combining residential real estate representation with expert mortgage services. This integrated approach removes the friction between finding a home and securing its financing. With over two decades of local expertise serving Santa Clara County, we act as an ethical anchor in a competitive industry, ensuring every step of your journey is handled with transparency and professional poise.

Our commitment to your success goes beyond a simple credit check. We understand that high-stakes transactions in Silicon Valley require a sense of reliability and a personal touch. By streamlining the journey from the initial underwritten review to the final closing signature, we provide a steady, purposeful rhythm that alleviates the stress of the market. We prioritize long-term relationships over quick transactions, positioning ourselves as a steadfast guide for both first-time participants and seasoned professionals.

Why a Local Broker Outperforms National Banks

National “big box” lenders often treat Silicon Valley buyers as just another data point in a queue. They frequently overlook the nuances of tech-sector income or the rapid pace of local negotiations. Working with our team provides direct access to Maria Elena ‘Nena’ Arriaga and a dedicated regional group that understands the heartbeat of San Jose. Local listing agents recognize our name, often viewing offers backed by our firm with a higher level of trust because they know our files are thoroughly vetted.

We offer customized loan products, including specialized jumbo loan origination and conventional processing, that are specifically tailored to the high-balance requirements of our region. This local credibility is often the deciding factor in a multiple-offer scenario. While national banks might struggle with the complexity of RSUs or the speed of an 11-day market, our team excels by providing efficient, ethical, and highly personalized service.

Start Your San Jose Home Journey Today

Your path to homeownership should be defined by certainty. We’ve refined the process of how to get pre-approved for a mortgage in san jose into a collaborative experience that puts you in control. Your first 30 minutes with our team will focus on a complimentary strategy session where we map out your financial goals and timeline. We’ll discuss your buying power and identify the best loan programs to fit your personal narrative.

We invite you to experience a mortgage process that values the human story behind the physical asset. Our team is ready to help you navigate the complexities of Santa Clara County with confidence and ease. Get pre-approved with Integrity Estates Realty today and take the first step toward securing your future in one of the world’s most vibrant communities.

Your Path to Silicon Valley Homeownership

Your journey to a new home in Silicon Valley begins with a strategic foundation. By mastering how to get pre-approved for a mortgage in san jose, you’ve moved beyond the uncertainty of the browsing phase and into a position as a serious, verified contender. You now understand that documentation for RSUs and the nuances of jumbo loan limits are not just hurdles; they’re opportunities to showcase your financial strength to local sellers. This preparation ensures you can act with speed and precision when the right property appears.

Integrity Estates Realty brings over 20 years of California real estate and mortgage experience to your side. We provide direct access to wholesale lender rates and possess deep expertise in navigating the complex income profiles of the tech sector. Our team is dedicated to providing the transparency and ethical conduct you need for a truly peace-of-mind transaction. Secure your San Jose mortgage pre-approval with Integrity Estates Realty. We look forward to helping you turn your vision of a Santa Clara County home into a reality.

Frequently Asked Questions

How long does a mortgage pre-approval last in San Jose?

A mortgage pre-approval typically remains valid for 60 to 90 days. This timeframe provides a window for you to shop with confidence, though you’ll need to provide updated pay stubs or bank statements if your search extends beyond this period. If market interest rates shift significantly, we may need to refresh your numbers to ensure your buying power remains accurate for the current landscape.

Does getting pre-approved for a mortgage hurt my credit score?

The pre-approval process requires a hard credit inquiry, which may cause a minor, temporary dip in your credit score, usually by fewer than five points. However, this is a necessary step to establish your credibility with sellers in a competitive market. Multiple inquiries for a mortgage within a short window are typically treated as a single event by credit bureaus, protecting your overall financial profile while you shop for rates.

Can I get pre-approved for a mortgage if I am self-employed in San Jose?

Yes, self-employed individuals can certainly qualify, provided they can document stable income through two years of federal tax returns and current profit and loss statements. Lenders look for consistency in your earnings to ensure you can manage the high-balance loans common in Santa Clara County. We specialize in analyzing complex business structures to help you understand how to get pre-approved for a mortgage in san jose.

What is the minimum credit score for a mortgage in Santa Clara County?

Minimum credit score requirements vary by loan program, starting at 580 for FHA loans and typically 620 for conventional financing. However, for the jumbo loans often required in San Jose’s $1.5 million market, most lenders look for a score of 700 or higher. Achieving a higher score often unlocks more favorable interest rates, which is vital for maintaining long-term value in a high-cost area.

How much house can I afford in San Jose based on my income?

Lenders generally look for a debt-to-income (DTI) ratio below 43%, though many Silicon Valley buyers aim for 36% to remain financially comfortable. Your affordability is calculated by looking at your gross monthly income against your existing debts and the projected housing payment. We help you balance this financial logic with your lifestyle aspirations to find a price point that supports your long-term goals.

What happens if my pre-approval amount is lower than the home prices in my desired neighborhood?

If your pre-approval falls short of local prices, we can explore several strategic adjustments. You might consider adding a co-signer, increasing your down payment through gift funds, or focusing on different loan products like high-balance conventional options. We work closely with you to refine your financial profile, ensuring you’re positioned to compete in neighborhoods like Willow Glen or Almaden Valley.

Can I use RSU income to qualify for a mortgage in San Jose?

Restricted Stock Units (RSUs) are a standard part of tech compensation and can be used to qualify if you have a two-year history of receiving them. You’ll need to provide your vesting schedule and grant letters to prove the income is stable and likely to continue. Understanding how to get pre-approved for a mortgage in san jose with stock-based pay is a core part of our local expertise.

How long does the pre-approval process take with Integrity Estates Realty?

The timeline for a fully underwritten pre-approval generally takes between three to five business days once all documentation is submitted. While some platforms offer instant letters, our methodical approach ensures your approval is respected by listing agents who demand verified data. This thoroughness provides the peace of mind needed for high-stakes Silicon Valley transactions, ensuring you’re ready to close without delays.