VA Loan Funding Fee in California: 2026 Rates, Exemptions, and Local Guide

In the high-stakes environment of the California real estate market, the VA funding fee isn’t just another line item on a closing statement; it’s a strategic variable that can define the long-term value of your home investment. You’ve likely noticed that the state’s soaring property values make every upfront cost feel magnified, especially when you’re trying to distinguish between first-time and subsequent use rates. Understanding the VA loan funding fee california is essential for any veteran looking to maximize their hard-earned benefits without overextending their finances in a competitive landscape.

We believe the path to homeownership should feel like a reward for your service, not a source of overwhelming stress. You deserve a clear, transparent look at how these costs settle into your 2026 mortgage plan. This article promises to clarify exactly how the funding fee impacts your purchase and how you might qualify to waive or reduce it. We’ll walk through the updated 2026 rate structures, detail specific disability exemptions, and show you how local expertise can help you navigate the nuances of the Golden State with complete peace of mind.

Key Takeaways

- Understand why this mandatory fee exists and how it serves as a strategic alternative to the recurring cost of monthly Private Mortgage Insurance (PMI).

- Navigate the specific 2026 rate structure for the VA loan funding fee california, including how your down payment amount can lower your total costs.

- Determine if you qualify for a full fee waiver through service-connected disability ratings or other specific military service exemptions.

- Learn how to manage financing in high-cost regions like Santa Clara and Monterey where property values require a sophisticated approach to loan limits.

- Explore the advantages of an integrated real estate and mortgage brokerage model to simplify your journey toward California homeownership.

What is the VA Funding Fee and Why Does it Exist?

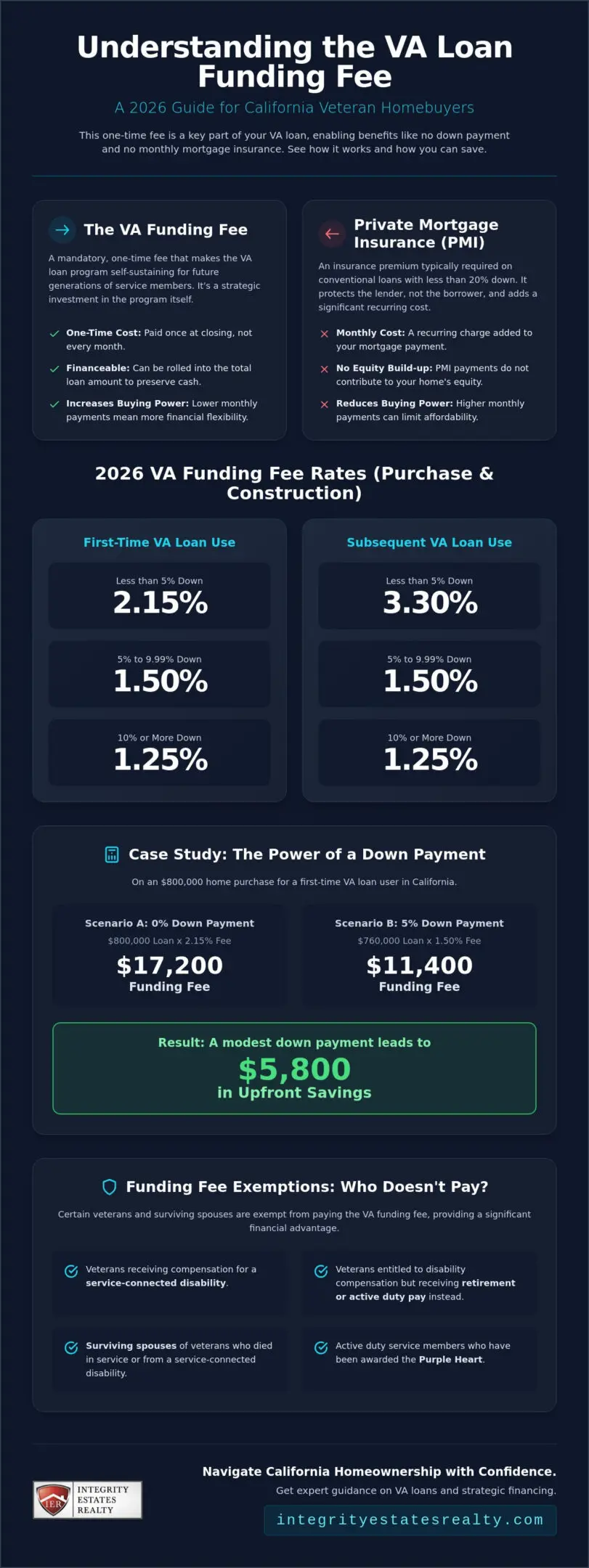

The VA loan program stands as a cornerstone of military benefits, offering a unique path to homeownership that bypasses many traditional financial hurdles. Central to this program is the funding fee, a mandatory federal requirement that ensures the initiative remains fiscally sustainable for future generations of service members. To understand What is the VA Funding Fee and Why Does it Exist?, one must view it as the primary mechanism that allows the Department of Veterans Affairs to guarantee these loans without requiring monthly mortgage insurance or a down payment. This fee isn’t a hidden cost or a penalty. It’s a strategic contribution to a self-sustaining system that has empowered millions of veterans to secure a place to call home. For those calculating the VA loan funding fee california, it represents a one-time investment into a program that provides long-term stability and unmatched borrowing power.

VA Funding Fee vs. Private Mortgage Insurance (PMI)

Traditional conventional loans typically require Private Mortgage Insurance if the buyer provides less than a 20% down payment. This monthly expense can add hundreds of dollars to a mortgage payment, especially in high-value markets like San Jose or San Francisco. The VA funding fee eliminates this recurring burden entirely. By opting for a one-time fee instead of a monthly insurance premium, California homeowners enjoy significantly better monthly cash flow. This financial flexibility is particularly valuable in the Golden State, where the high cost of living demands precise and intentional budgeting. Over the life of a thirty-year loan, the absence of PMI often results in tens of thousands of dollars in savings, proving that the funding fee is a far more efficient model for the veteran borrower.

How the Fee is Collected

Transparency is a core value in our approach to real estate and lending. During the initial loan disclosure process, the exact amount of your funding fee will be clearly outlined so there are no surprises at the finish line. Most borrowers choose to “roll” the fee into the total loan amount rather than paying it as an upfront closing cost. While this slightly increases the total loan balance, it preserves your liquid cash for other essential needs, such as moving expenses or personalizing your new space. The VA funding fee serves as a strategic substitute for traditional mortgage insurance. Whether you pay it at closing or finance it over the term of the mortgage, this fee remains a key component of the VA loan funding fee california landscape, providing the security needed to maintain this vital benefit for every hero who calls this state home.

2026 VA Funding Fee Rates for California Homebuyers

Securing a home in the California market requires a clear understanding of the financial landscape, particularly as rates evolve. For 2026, the VA loan funding fee california remains a central component of the closing process. If you’re using your benefit for the first time with a 0% down payment, the fee is set at 2.15% of the total loan amount. This percentage increases to 3.3% for subsequent use. The higher rate for repeat users exists to ensure the program stays robust and available for future veterans, reflecting a collective investment in the community of service members. While these percentages may seem small, they translate into significant figures when applied to the high property values found throughout the state.

Purchase and Construction Loan Rates

The total cost of your funding fee is directly influenced by your initial equity position. By providing a down payment, you can trigger substantial reductions in these rates. For both first-time and subsequent users, a down payment between 5% and 9.99% reduces the fee to 1.5%. If you’re able to contribute 10% or more, the fee drops further to 1.25%. Consider a hypothetical purchase of an $800,000 home in Gilroy. With 0% down as a first-time user, the fee would be $17,200. However, by providing a 5% down payment of $40,000, the fee on the remaining $760,000 loan balance falls to $11,400. This strategic move saves you $5,800 upfront, illustrating how even a modest down payment can alter your long-term financial trajectory. You can learn more about specific eligibility and VA Funding Fee Exemptions: Who Doesn’t Have to Pay? to see if these costs apply to your situation.

Refinancing Rates: IRRRL and Cash-Out

For veterans who already own property, 2026 offers efficient pathways to lower interest rates or access home equity. The Interest Rate Reduction Refinance Loan (IRRRL), often called a VA Streamline, carries a minimal fee of just 0.5%. This is a powerful tool for California homeowners aiming to reduce monthly obligations with minimal paperwork. Conversely, if you’re looking to leverage your home’s value for debt consolidation or improvements, a Cash-Out Refinance follows the standard purchase rates of 2.15% for first-time use and 3.3% for subsequent use. For a deeper dive into these options, our Refinance Mortgage Gilroy guide provides a comprehensive look at maximizing your equity. Balancing these costs requires a partner who understands the local market nuances. Our team at Integrity Estates Realty is here to help you evaluate which path aligns best with your personal narrative and financial goals.

VA Funding Fee Exemptions: Who Doesn’t Have to Pay?

While the VA loan funding fee california is a standard requirement for many, a significant number of veterans qualify for a total waiver of this cost. This isn’t merely a minor discount. It’s a substantial financial advantage that can save you tens of thousands of dollars, especially when navigating the premium price points of the California market. Understanding these exemptions is the first step in ensuring you aren’t overpaying for your home. You can review the official VA Funding Fee rates and exemption criteria to see how they align with your specific service history and current status.

The primary exemption applies to veterans who receive VA compensation for a service-connected disability. This also extends to veterans who would be entitled to receive compensation for a service-connected disability if they weren’t receiving retirement pay or active-duty pay instead. Additionally, the fee is waived for surviving spouses of veterans who died in service or from a service-connected disability, provided they are receiving Dependency and Indemnity Compensation (DIC). Active-duty service members who have been awarded the Purple Heart also stand exempt from this requirement. Finally, service members who have a proposed or memorandum rating before the loan closing date, stating they are eligible for compensation due to a pre-discharge claim, can often have the fee removed from their closing costs.

The Role of the Certificate of Eligibility (COE)

Your Certificate of Eligibility (COE) acts as the definitive verification of your status for your lender. It’s the foundational document that confirms whether you’re required to pay or if you’ve earned an exemption. The VA funding fee is waived for any veteran receiving compensation for a service-connected disability. If your disability claim is currently pending at the time of your loan closing, don’t lose heart. While you may need to pay the fee initially to keep your closing on schedule, the status of your claim at the moment the loan is finalized is what ultimately determines your liability. We often work with veterans to ensure their COE is updated and accurate before the final papers are signed, providing a sense of security throughout the process.

How to Claim a Refund

There are instances where a disability rating is granted retroactively, dating back to a period before your home loan closed. In these cases, you’re entitled to a full refund of the VA loan funding fee california you paid or financed. The process involves submitting a formal request to the VA, supported by your rating decision letter and loan documents. There are specific time limits for these claims, typically tied to the effective date of your disability award. A local mortgage broker can be a steadfast guide in this scenario, helping you gather the necessary documentation and communicating with the VA on your behalf. This collaborative partnership ensures that every benefit you’ve earned is fully realized, protecting your home’s equity and your family’s financial future.

Navigating VA Loans in High-Cost California Counties

California’s geography presents a unique financial puzzle for veterans. In counties like Santa Clara or Monterey, where entry-level home prices often exceed the national average by double or triple, the math behind the VA loan funding fee california requires extra precision. For a veteran with full entitlement, the VA no longer imposes a maximum loan limit, allowing you to purchase a high-value property with zero down payment. However, while the loan amount is uncapped, the funding fee scales proportionally. Rolling a 3.3% subsequent-use fee into a $1.1 million mortgage in the Bay Area adds over $36,000 to your loan balance. This is a significant sum. It demands a thoughtful strategy before signing the final disclosures.

For those with partial entitlement, the 2026 loan limits in high-cost counties like San Francisco and San Jose reach up to $1,149,825. Navigating these higher thresholds means the funding fee becomes a larger part of your overall debt-to-income calculation. While the fee replaces monthly mortgage insurance, the sheer size of the loan in Silicon Valley or Salinas means that even a small percentage point change can alter your monthly payment by hundreds of dollars. It’s essential to look at the total cost of borrowing over the first five to ten years to truly understand the impact of your financing choices.

Strategies for High-Value Transactions

One of the most effective ways to manage these costs is to aim for the 5% down payment tier. In a high-cost market, contributing 5% might seem daunting; yet, it triggers a reduction in the fee to 1.5% for both first-time and subsequent users. This reduction often pays for itself within a few years through reduced interest and principal. If you’re weighing this against other low-down-payment options, our guide on FHA Home Loans in Gilroy provides a detailed comparison of government-backed programs. In high-appreciation areas like San Jose or Salinas, many veterans find that paying the fee upfront is the best path to maximizing equity growth. The break-even point usually occurs when the home’s appreciation outpaces the initial cost of the fee within the first few years of ownership.

Local Market Factors: San Francisco to Fresno

The financing needs of a buyer in the tech hubs of San Francisco or San Jose differ wildly from those looking in the Central Valley cities of Modesto, Turlock, or Fresno. Local appraisal knowledge is critical here. An appraiser who understands the specific nuances of the Gilroy Real Estate Market Trends can ensure your high-value transaction reflects the true worth of the property, which is vital when calculating your final loan-to-value ratio. Whether you’re eyeing a suburban retreat in Salinas or a modern listing in Silicon Valley, the regional context matters. We invite you to connect with our team at Integrity Estates Realty to receive a personalized analysis of how these county-specific factors influence your purchase power. Balancing high-balance loans with the right fee structure is our specialty. We ensure your journey is guided by data and local pride.

Strategic Financing with Integrity Estates Realty

Choosing the right home is a lifestyle decision. Financing it is a financial strategy. At Integrity Estates Realty, we bridge the gap between these two worlds by operating as both a premier real estate agency and a sophisticated mortgage brokerage. This dual-threat approach is specifically designed to alleviate the friction often found in the VA loan funding fee california process. When your real estate representative and your loan officer are on the same team, communication is seamless. We don’t just find you a property; we architect a financing plan that respects your service and protects your equity from the very first day.

The Advantage of an Integrated Brokerage

Our service area stretches from the vibrant neighborhoods of Sacramento down to the fertile landscapes of Fresno. By offering in-house VA Loan Origination alongside residential representation, we provide a level of oversight that traditional, fragmented models cannot match. You won’t have to explain your financial goals to two different companies. Instead, you’ll have a steadfast guide who understands how the specific details of a listing in Salinas or Gilroy will impact your final loan disclosures and funding fee calculations. This integration reduces the administrative burden on your family, allowing you to focus on the excitement of your move rather than the stress of the paperwork.

One of the most critical decisions you’ll face is whether to pay the funding fee upfront or roll it into your mortgage. In high-appreciation markets like Silicon Valley or Monterey County, financing a 3.3% fee on a high-balance loan means you’re paying interest on that fee for the next thirty years. For some veterans, paying the fee at closing is the superior financial choice to maximize long-term wealth and equity growth. We provide the data-driven analysis you need to make this decision with total confidence, ensuring your loan-to-value ratio remains healthy even as property values fluctuate.

Your Next Steps to a VA Home Loan

Maria Elena ‘Nena’ Arriaga brings over twenty years of ethical local experience to every transaction. Her dedication to transparency and reliability has made our brand an anchor for veterans throughout the region. We understand that a home is more than a physical asset; it’s a personal dream and a place of belonging. Our personality is rooted in high-minded dedication, and we prioritize your long-term peace of mind over quick transactions.

We invite you to a personalized consultation where we can review your Certificate of Eligibility together. We’ll determine if you qualify for a full exemption or if a strategic down payment can lower your 2026 rates. Our goal is to ensure you feel like a partner, not just a participant, in your home-buying journey. Contact Integrity Estates Realty today for a personalized VA loan consultation.

Secure Your Future with Confidence and Local Expertise

Navigating the VA loan funding fee california is more than just a calculation; it’s a strategic step toward securing your legacy in the Golden State. We’ve explored how the 2026 rate structure rewards proactive planning, especially through the 5% down payment tier, and how vital exemptions can entirely eliminate these costs for eligible heroes. Whether you’re eyeing a high-value property in Santa Clara or a family home in Salinas, understanding these nuances ensures you never pay more than necessary.

You don’t have to manage this journey alone. With over 20 years of California real estate and mortgage experience, our veteran-friendly brokerage serves more than 20 cities with a commitment to transparency and ethical conduct. We provide integrated real estate and mortgage services to create a seamless, stress-free experience tailored to your unique narrative. Start Your VA Loan Journey with Integrity Estates Realty and let us guide you home. Your service has earned you this benefit, and we’re honored to help you maximize it.

Common Questions Regarding the VA Funding Fee in California

Can I roll the VA funding fee into my monthly mortgage payment?

You can absolutely roll the VA funding fee into your total loan amount rather than paying it as an upfront closing cost. This common practice means the fee is amortized over the life of your mortgage, effectively becoming part of your monthly principal and interest payments. While this preserves your liquid cash for moving expenses in high-cost areas, it does slightly increase your total loan balance and the interest paid over the life of the loan.

Is the VA funding fee tax-deductible in California in 2026?

The VA funding fee remains tax-deductible for California homeowners as of 2026. Because the IRS generally treats this fee as a form of mortgage insurance, you can typically deduct the full amount in the year it was paid or over the term of the mortgage if it was financed. We recommend consulting with a qualified tax professional to ensure you maximize this benefit based on your specific income level and filing status.

Do I have to pay the funding fee again if I use a VA loan a second time?

You’re required to pay the fee for each subsequent use of your benefit, though the rate increases to 3.3% for a zero-down purchase. This higher cost reflects the ongoing investment needed to sustain the program for all veterans. However, you can reduce this rate to 1.5% or 1.25% by providing a down payment of 5% or 10% respectively, making subsequent use more affordable in competitive California markets.

How much is the VA funding fee for a 0% down purchase in Santa Clara County?

For a first-time home purchase with 0% down in Santa Clara County, the VA loan funding fee california is set at 2.15% of the total loan amount. Given the high property values in San Jose and surrounding cities, this percentage can represent a significant figure. For instance, on a $900,000 loan, the fee would be $19,350. Our team helps you analyze whether rolling this into your high-balance loan aligns with your long-term equity goals.

What happens if my VA disability rating is approved after my loan closes?

If your service-connected disability rating is granted retroactively to a date before your loan closing, you are eligible for a full refund of the fee. You’ll need to submit your rating decision letter and final closing disclosure to the VA for processing. We often assist our clients in coordinating with the Department of Veterans Affairs to ensure these funds are returned promptly, which can then be applied to your principal balance or returned as cash.

Are there any local California grants that can help pay the funding fee?

While the federal government manages the funding fee, the state offers unique support through the CalVet Home Loan program and the proposed Veterans and Affordable Housing Bond Act of 2026. These initiatives aim to increase affordability and may provide alternative financing structures that help mitigate upfront costs. Local programs vary by county, so it’s wise to check for specific municipal housing grants in areas like Fresno or Sacramento that support veteran homeownership.

How does the VA funding fee compare to FHA mortgage insurance premiums?

The VA funding fee is a one-time cost, whereas FHA loans require both an upfront premium and a recurring monthly mortgage insurance premium (MIP). For most California veterans, the VA option provides superior monthly cash flow because it lacks that monthly insurance burden. Over several years, the savings from avoiding monthly MIP typically far outweigh the initial VA loan funding fee california, especially on the larger loan amounts common in the Golden State.

Can the seller pay the VA funding fee for me in California?

Sellers in California are permitted to pay the VA funding fee on your behalf as part of their allowable concessions. The VA allows sellers to contribute up to 4% of the total loan amount toward the buyer’s closing costs, which can include the funding fee, prepaid taxes, and insurance. In a shifting market, negotiating for the seller to cover this fee is a sophisticated strategy to keep your out-of-pocket costs at a minimum while securing a high-value property.