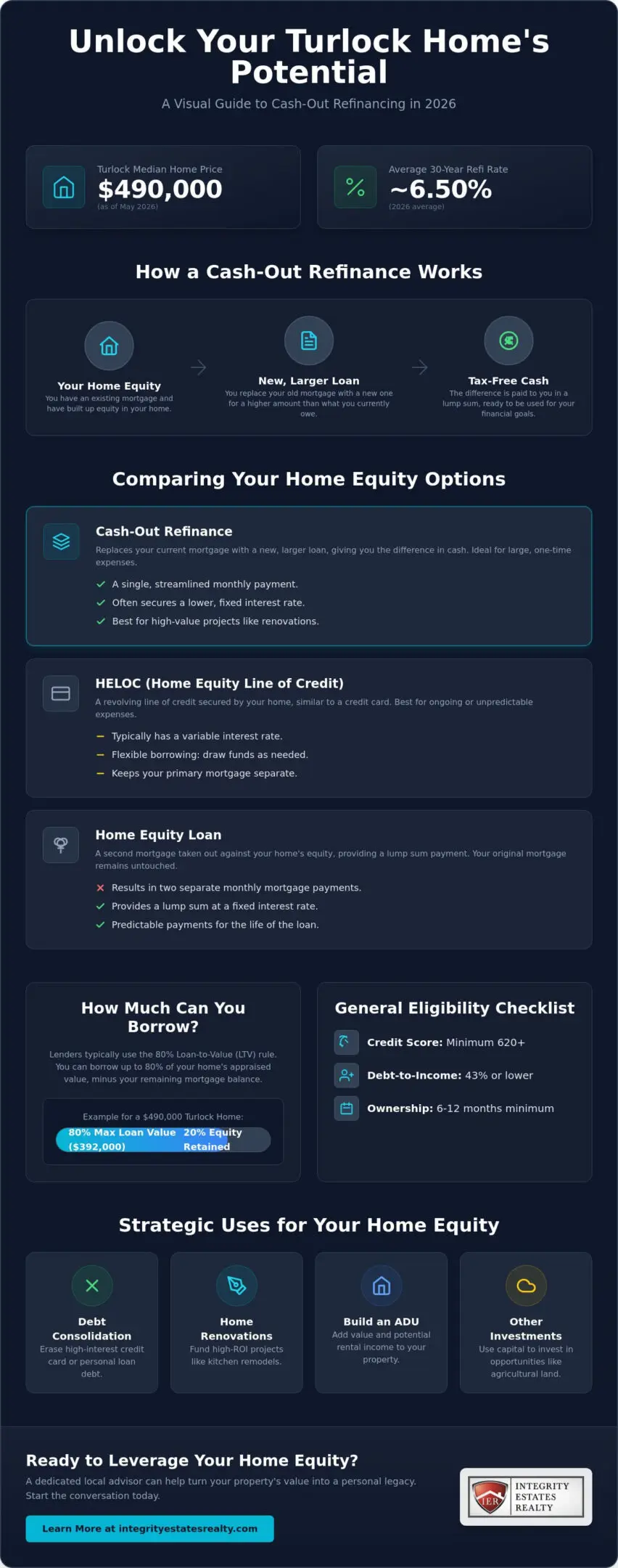

Cash-Out Refinance in Turlock, CA: The 2026 Homeowner’s Guide to Equity

What if the equity sitting in your Turlock home isn’t just a static figure on a balance sheet, but the bridge to erasing high-interest debt and finally building that ADU? With the median home listing price in Turlock holding at $490,000 as of May 2026, many local homeowners are sitting on a goldmine of untapped potential. You’ve likely felt the sting of a rising cost of living in the Central Valley, where high-interest credit card debt and the need for modernizations can make financial peace feel elusive. It’s a common stressor, but your home remains your most powerful asset.

This guide explains how a cash out refinance turlock ca can serve as a strategic wealth-management tool rather than just another loan. You’ll learn how to leverage current 2026 market dynamics, where 30-year fixed refinance rates are averaging around 6.50 percent, to secure the capital needed for renovations or debt consolidation. We will walk through the specific requirements for Turlock properties and show you how a collaborative partnership with a local expert can turn your property’s value into a personal legacy. We’ll preview the steps to lowering your monthly obligations and funding the projects that matter most to your family’s future.

Key Takeaways

- Learn how your Turlock home’s steady appreciation can be converted into liquid capital for debt consolidation or significant property modernizations.

- Explore the 2026 eligibility standards, including credit scores and debt-to-income ratios, required for a successful cash out refinance turlock ca.

- Identify strategic, high-ROI projects like kitchen remodels or ADUs that maximize your home’s value while improving your daily lifestyle.

- Gain a clear understanding of the refinancing timeline, from the initial expert consultation to the final disclosure of your loan estimate.

- Discover the benefits of working with a dedicated local advisor who prioritizes your long-term financial health over simple transactions.

Understanding Cash-Out Refinancing for Turlock Homeowners

A cash-out refinance involves replacing your existing mortgage with a new, larger loan. You receive the difference between the two loans in a lump sum of cash at closing. Unlike a traditional rate-and-term refinance, which only changes your interest rate or loan duration, a cash out refinance turlock ca allows you to tap into the wealth you’ve built in your property. Many local families find this particularly attractive in 2026, as property values in the Central Valley have shown remarkable resilience compared to more volatile coastal markets. This financial tool transforms your home from a simple residence into a versatile source of capital.

While there are several ways to access home equity, each serves a different purpose. Understanding the nuances helps you choose the path that aligns with your lifestyle goals. Local homeowners often compare these three common options:

- Cash-Out Refinance: This replaces your primary mortgage with a single new loan. It often provides a lower interest rate than secondary financing and keeps your monthly obligations streamlined into one payment.

- HELOC (Home Equity Line of Credit): This functions like a credit card secured by your home. It’s useful for ongoing expenses, though it typically carries a variable interest rate that can fluctuate with the market.

- Home Equity Loan: This is a second mortgage that provides a lump sum at a fixed rate. It’s a solid choice if you don’t want to touch your original mortgage, but it does result in two separate monthly payments.

In Turlock, homeowners frequently prioritize a cash-out refinance to fund high-value kitchen modernizations or to invest in local agricultural land. By consolidating the debt into a primary mortgage, they often secure more favorable terms while fueling their long-term financial growth.

How Equity is Calculated in the Turlock Market

Equity is the difference between the current market value of your home and your remaining mortgage balance. In Stanislaus County, lenders typically adhere to the 80 percent Loan-to-Value (LTV) rule. This means you can generally borrow up to 80 percent of your home’s appraised value, minus what you still owe. For example, if your home is valued at the May 2026 Turlock median listing price of $490,000, your total loan amount would typically be capped at $392,000. This buffer ensures you retain a 20 percent stake in your property, protecting your financial stability even if market conditions shift.

Why 2026 is a Strategic Year for Turlock Refinancing

The Turlock housing market remains a pillar of stability within California. While the median listing price saw a 7.55 percent year-over-year decrease as of May 2026, the market remains characterized by low inventory, with only 187 active listings during that same period. This scarcity helps maintain appraised values, giving homeowners a solid foundation for refinancing. Local economic drivers further bolster this confidence. The presence of California State University, Stanislaus, provides a steady anchor for housing demand, while our region’s robust agricultural sector continues to fuel growth. These factors create a unique environment where property isn’t just a place to live; it’s a versatile financial asset. Accessing your equity now allows you to stay ahead of rising costs while reinvesting in a community that continues to thrive.

Eligibility and Requirements for a Turlock Refinance

Securing a cash out refinance turlock ca requires more than just home equity. Lenders in Stanislaus County look at your full financial profile to ensure the new loan is sustainable for your long-term goals. Generally, you’ll need a minimum credit score of 620 for a conventional refinance. If your score is lower, FHA options may provide a path forward, though they often come with different insurance requirements. Beyond your score, your debt-to-income (DTI) ratio is a primary factor. Most lenders prefer a DTI of 43 percent or lower to ensure you aren’t overextended by your monthly obligations.

Seasoning requirements also apply to your property. In most cases, you must have owned your Turlock home for at least six to twelve months before you can tap into its equity. When you’re ready to apply, gathering your documentation early prevents delays. You’ll need recent W-2s, pay stubs, and tax returns. Because Turlock is part of a unique agricultural and suburban landscape, providing your most recent property tax assessment from the Stanislaus County Assessor’s Office can also help streamline the underwriting process. If you are unsure where your current profile stands, reviewing your goals with a professional local broker can provide the clarity you need before you begin the formal application.

Credit Score Benchmarks for Turlock Borrowers

Credit scores act as a gatekeeper for the most favorable interest rates. While a score of 620 is the baseline for many conventional programs, borrowers with scores above 740 often unlock the lowest possible costs. This is particularly relevant if you’re pursuing a Jumbo loan, which may be necessary if your loan amount exceeds the 2026 conforming limit of $1,209,750 in high-cost California regions. Government data on refinancing suggests that many homeowners successfully use these funds to pay off high-interest credit cards, which can actually lead to a higher credit score over time. If your score is currently on the edge, consider paying down small revolving balances thirty days before your lender pulls your credit report.

The Importance of a Turlock-Specific Appraisal

The success of your refinance often hinges on a precise appraisal. An appraiser who understands the nuances of Northeast Turlock or the historic charm of Monte Vista will provide a more accurate valuation than someone from outside the area. They select “comps” (comparable sales) directly from the Stanislaus County MLS, looking for homes with similar square footage and upgrades that have sold within the last six months. To maximize your value, ensure your home is well-maintained for the inspection. Simple steps like tidying the landscaping, finishing minor repairs, and providing a list of recent upgrades can help the appraiser see the full value of your investment.

Strategic Uses for Your Home Equity in 2026

Home equity represents years of hard work and disciplined payments. In 2026, savvy homeowners view this equity as a strategic reserve for lifestyle curation and wealth building. Utilizing a cash out refinance turlock ca provides the liquidity needed to tackle high-ROI projects that maintain your property’s competitive edge. Adding an Accessory Dwelling Unit (ADU) is a particularly smart move in our community. With the local student population at CSU Stanislaus constantly seeking quality housing, an ADU can generate monthly rental income that offsets your new mortgage payment. Kitchen modernizations also remain a top priority, as they significantly boost resale value in a market where buyers favor move-in-ready homes.

Beyond physical structures, equity can fund the milestones that define a family’s legacy. This might include covering tuition costs for a child attending CSU Stanislaus or providing the seed money for a long-term family investment. Your home serves as a bridge to these opportunities, allowing you to access capital without depleting your liquid savings or emergency funds. It’s about turning a static asset into a dynamic tool for your family’s future.

Debt Consolidation: A Path to Financial Peace of Mind

The rising cost of living in the Central Valley has led many to rely on high-interest credit cards for daily expenses. In 2026, credit card interest rates can often triple the cost of a standard mortgage. By consolidating these balances into a single mortgage payment at a rate near 6.50 percent, you drastically reduce your monthly interest outflow. This isn’t just about the numbers; it’s about the psychological relief of a simplified financial life. Instead of managing multiple due dates and compounding interest, you have one predictable payment. While you should consult a tax professional regarding the deductibility of mortgage interest, the immediate cash flow improvement is often a game-changer for Turlock families.

Investing in Turlock Real Estate

Your primary residence can be the springboard for a larger investment portfolio. Many local owners use their equity as a down payment for commercial opportunities or additional residential units. This strategy allows you to diversify your assets within the local Stanislaus County area or expand into nearby markets like commercial real estate in Gilroy. When calculating your “break-even” point, consider the potential rental income against the cost of the larger mortgage. This methodical approach ensures your home equity is working as hard for your future as you did to earn it. By leveraging the value you’ve already built, you can secure a position in the growing Central Valley economy.

The Turlock Refinance Process: A Step-by-Step Guide

The journey toward a cash out refinance turlock ca begins with a purposeful consultation. This initial stage isn’t just a paperwork review; it’s a collaborative session where we align your financial aspirations with the current market realities of Stanislaus County. Once your goals are clear, the formal application follows. Within three business days, you’ll receive a Loan Estimate (LE). This document provides a transparent breakdown of your interest rate, monthly payments, and estimated closing costs, giving you the clarity needed to move forward with confidence.

Next, the process moves into the technical phase of appraisal and underwriting. As we discussed earlier, a local appraiser’s knowledge is vital for capturing the true value of Turlock neighborhoods like Monte Vista. While the appraiser evaluates the property, the underwriter reviews your financial documentation to confirm everything meets 2026 lending standards. Once the file is approved, you reach the closing table to sign your final documents. After a short waiting period, the funds are disbursed directly to you.

Navigating Closing Costs in Turlock

Transparency is the cornerstone of a reliable partnership. During a refinance, you’ll encounter fees for title insurance, escrow services, and county recording. Some homeowners are drawn to “no-cost” refinance offers, but it’s a myth that these fees simply disappear. In these scenarios, the costs are usually rolled into the principal balance or exchanged for a slightly higher interest rate. In the current 2026 market, closing costs for a cash-out refinance typically range from 2 percent to 5 percent of the total loan amount. Understanding these nuances upfront prevents surprises at the final signing. If you’re ready to review your specific numbers, you can start your refinance application today with our expert team.

Timeline: From Application to Cash-in-Hand

Efficiency matters when you have a project waiting. In the 2026 Turlock market, the average processing time from application to funding generally spans 30 to 45 days. Several factors can influence this pace, including the speed of the appraisal and how quickly you provide requested documentation. Once you sign your final closing documents, California law mandates a “Right of Rescission” period. This is a three-day window that allows you to cancel the transaction for any reason. After this cooling-off period expires, the funds are disbursed, providing the capital you need for your next big investment or renovation.

Why Work with Integrity Estates Realty for Your Turlock Refinance?

Choosing a partner for a high-stakes transaction like a cash out refinance turlock ca requires more than just comparing interest rates on a screen. It demands a guide who values your long-term financial health as much as you do. At Integrity Estates Realty, we’ve spent over two decades serving Turlock and the greater Central Valley. This deep-rooted experience has allowed us to refine a sophisticated, professional approach that balances the authoritative voice of market experts with the warm, personal touch of a dedicated advisor. We don’t view our clients as transactions; we view them as neighbors whose success contributes to the strength of our entire community.

Our unique position as both a real estate agency and a mortgage brokerage provides a seamless service that few can match. This dual expertise means we understand the physical value of your property as well as the intricate financial mechanisms required to leverage it. We eliminate the friction often found when working with separate entities, ensuring that your appraisal, underwriting, and closing processes are handled with a unified strategy. Our core brand promise is built on transparency and ethical conduct, serving as an anchor in a competitive industry where quick sales often overshadow long-term stability.

Your Local Turlock Mortgage Partner

Local pride is the engine behind our results. We understand the nuances of the Turlock landscape, from the quiet residential streets near CSU Stanislaus to the sprawling agricultural properties on the outskirts of town. This familiarity allows us to position your refinance in the best possible light for lenders. We maintain an extensive network of wholesale lenders, which gives our clients access to competitive 2026 rates that might not be available through traditional retail banks. For those with property interests throughout the region, our refinance mortgage Gilroy guide offers broader insights into how we support homeowners across the Central Valley and South Bay.

Start Your Turlock Equity Consultation Today

We operate under an “ethical anchor” philosophy. This means we only recommend a cash out refinance if it provides a genuine, documented benefit to your financial situation. Our goal is to alleviate the stress of high-stakes decisions by providing clear, honest communication at every turn. We invite you to schedule a personalized review where we can analyze your current mortgage, assess your home’s 2026 value, and discuss your lifestyle goals. Whether you’re ready to fund a major renovation or consolidate high-interest debt, we are here to guide you through the journey with purpose and precision. Contact Integrity Estates Realty today to explore the potential waiting within your Turlock home.

Empower Your Financial Future in Turlock

Your home is more than just a place to live; it’s the foundation of your financial security and a catalyst for your family’s aspirations. We’ve explored how a cash out refinance turlock ca can transform your property’s value into liquid capital for high-ROI renovations, debt consolidation, or strategic investments. By understanding the 2026 eligibility requirements and following a methodical process, you can navigate the complexities of the Central Valley market with confidence.

At Integrity Estates Realty, we’ve been serving California homeowners since 2004. Our integrated real estate and mortgage expertise ensures that your journey is guided by deeply rooted local Turlock market knowledge. We prioritize your long-term peace of mind, acting as an ethical anchor while you leverage your hardest-earned asset. Your vision for a modernized kitchen, a debt-free lifestyle, or a growing portfolio is within reach when you partner with experts who are as invested in your narrative as you are.

Ready to take the next step? Secure your Turlock home equity with Integrity Estates Realty and discover the possibilities waiting within your walls. We look forward to helping you turn your property’s potential into a lasting legacy.

Frequently Asked Questions

How much cash can I realistically get from a refinance in Turlock?

You can typically borrow up to 80 percent of your home’s appraised value. With Turlock’s median listing price at $490,000 as of May 2026, a homeowner with a $200,000 mortgage balance could potentially access up to $192,000 in cash. This calculation ensures you maintain a 20 percent equity stake, which preserves your financial stability and meets the standard lender requirements found across Stanislaus County.

Will a cash-out refinance increase my property taxes in Stanislaus County?

A standard cash-out refinance does not trigger a property tax reassessment in California. Under Proposition 13, your base year value remains the same regardless of your new loan amount. However, if you use the funds for major new construction, such as adding an ADU, the Stanislaus County Assessor will assess the value of that specific improvement. This could lead to a modest increase in your total annual tax bill.

Is a cash-out refinance better than a home equity line of credit (HELOC)?

A cash-out refinance is often superior for homeowners who prefer the security of a fixed interest rate and a single monthly payment. While a HELOC offers flexibility, it usually carries a variable rate that can rise unexpectedly as market conditions shift. If you are funding a large, one-time project like a kitchen remodel or consolidating high-interest debt, the stability of a primary mortgage refinance provides better long-term peace of mind.

What is the minimum credit score for a cash-out refinance in California in 2026?

Most lenders require a minimum credit score of 620 for a conventional cash out refinance turlock ca. Borrowers with scores above 740 typically qualify for the most competitive interest rates and lower closing costs. If your score falls below the 620 threshold, you might explore FHA options, though these programs often have specific insurance requirements that can impact the overall monthly cost of your new loan.

Can I use a cash-out refinance on an investment property in Turlock?

Yes, you can refinance investment properties, though lenders often apply stricter standards than they do for primary residences. You might be limited to a 70 percent or 75 percent loan-to-value ratio rather than the standard 80 percent. This is a common strategy for local investors looking to pull capital from one Turlock rental to fund the purchase of another commercial or residential property within the Central Valley.

How long does the cash-out refinance process take from start to finish?

The typical timeline spans 30 to 45 days from the initial application to the final disbursement of funds. Delays often stem from appraisal backlogs or incomplete documentation during the underwriting phase. To ensure an efficient experience, gather your W-2s, tax returns, and bank statements before your consultation. Once you sign the final documents, California law requires a three-day rescission period before the cash is deposited into your account.

Are there tax implications for the cash I receive from my refinance?

The cash you receive from a refinance is not considered income, so it is not subject to personal income tax. It is essentially a loan against your own asset rather than a windfall. However, the deductibility of the mortgage interest depends on how you use the funds. If the cash is used for home improvements, the interest may be deductible; it’s vital to consult a tax professional to review your specific situation.

What happens if my Turlock home appraises for less than I expected?

If the appraisal comes in low, the amount of cash you can withdraw will be reduced to stay within the 80 percent LTV limit. In some cases, you may need to adjust your project scope or bring cash to the table if you still wish to proceed with the loan. Working with a local expert who understands Turlock’s specific neighborhoods ensures the appraiser uses the most accurate comparable sales from the local MLS.