FHA Loan vs. Conventional in Gilroy: Which is Right for the 2026 Market?

What if the financing strategy that saved your neighbor thousands in 2024 is the very reason your offer gets rejected in the 2026 Gilroy market? You already understand that securing a sanctuary in Santa Clara County requires more than just a high bid. With the median home price in Gilroy expected to hold steady near $1,050,000, the pressure of competing against aggressive cash buyers is a reality we face together. It’s natural to feel a sense of hesitation when the stakes for your family’s legacy are this high.

At Integrity Estates Realty, we believe your path to homeownership should be built on a foundation of clarity and ethical guidance. We’ve compiled this expert comparison of an fha loan vs conventional gilroy buyers can use to gain a competitive edge. You’ll discover how to choose the right mortgage insurance structure and down payment strategy to ensure your offer stands out. We will examine the specific credit thresholds, long term equity implications, and seller expectations that will define the local real estate landscape over the next 12 months.

Key Takeaways

- Understand the critical nuances of an fha loan vs conventional gilroy to determine which financing path offers the most secure financial legacy in the 2026 market.

- Learn how specific credit score thresholds and down payment realities impact your accessibility to premium Silicon Valley real estate.

- Discover strategic ways to debunk seller myths and win bidding wars in competitive neighborhoods like Eagle Ridge and Las Animas.

- Evaluate the “True Cost” of your mortgage over time to decide if an FHA-to-Conventional refinance strategy aligns with your long-term wealth goals.

- Explore the unique advantage of an integrated real estate and mortgage partnership designed to provide a seamless, ethical home-buying journey.

Understanding FHA and Conventional Loans in the Gilroy Landscape

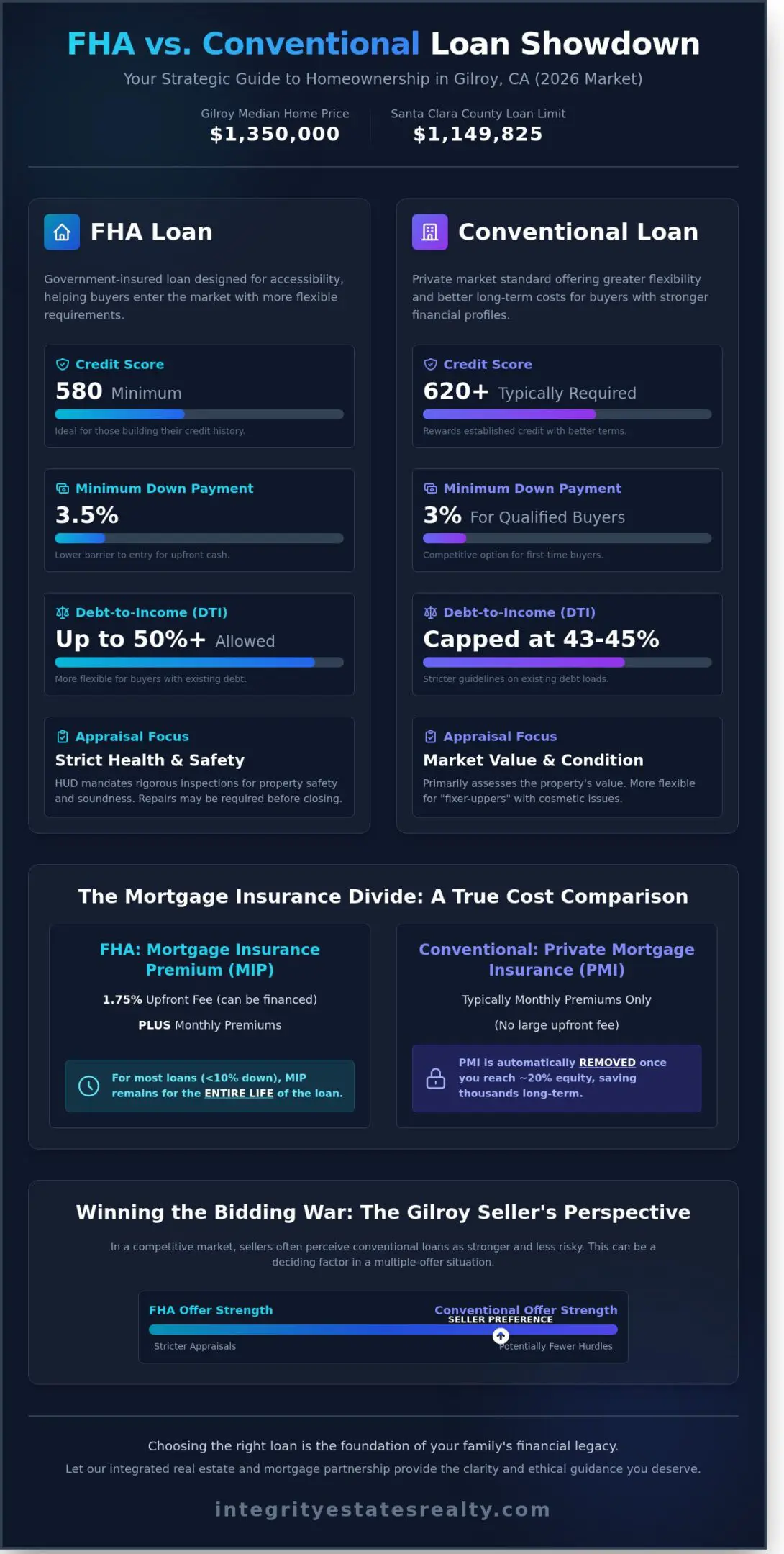

Choosing a mortgage in 2026 requires more than a simple credit check; it demands a strategy tailored to the unique pulse of Santa Clara County. As the median home price in Gilroy reaches $1.35 million this year, the decision between an fha loan vs conventional gilroy buyers face becomes a pivotal step in building a lasting legacy. At Integrity Estates Realty, we view this choice as the foundation of your financial sanctuary. We prioritize transparency and ethical guidance to ensure your home remains a source of peace rather than pressure. Understanding the specific mechanics of an fha loan vs conventional gilroy financing path is the first step toward a seamless transaction.

The Core Philosophy of FHA Financing

The Federal Housing Administration provides a safety net for those who might otherwise feel excluded from the California market. An FHA insured loan functions by protecting lenders against loss, which allows for more inclusive qualification standards. Borrowers with a credit score as low as 580 can secure a 3.5% down payment. Many local buyers mistakenly believe these loans are restricted to distressed properties. In reality, modern fha home loans gilroy programs support high-quality residences across Gilroy, from suburban estates to modern townhomes. It’s a reliable bridge for first-time buyers aiming to plant roots in our community without the burden of a massive upfront investment.

The Conventional Advantage in California

Conventional loans represent the private-market standard, governed by entities like Fannie Mae and Freddie Mac. These options offer significant flexibility for those with credit scores typically above 620. While a 20% down payment was once the benchmark, 2026 programs allow for as little as 3% down for qualified applicants. The primary advantage lies in the treatment of Private Mortgage Insurance (PMI). Unlike FHA premiums that often last for the life of the loan, conventional PMI can be removed once you reach 20% equity. This path accelerates your journey toward total ownership and long-term financial freedom, allowing your home to serve as a growing asset for your family. Veterans and active-duty service members may also want to explore va home loan benefits california residents can access, which offer a zero-down-payment alternative that bypasses mortgage insurance entirely.

Side-by-Side: Requirements and 2026 Loan Limits

Choosing between an FHA loan vs conventional Gilroy mortgage requires a clear understanding of how your financial profile aligns with federal and private standards. FHA loans prioritize accessibility, allowing for a credit score as low as 580 with a 3.5% down payment. Conventional loans demand more robust credit, typically requiring a 620 minimum; however, they offer a 3% down payment option specifically for qualified first-time buyers. This distinction often makes FHA the preferred path for those building their credit legacy, while conventional loans reward those with established scores through lower long-term costs.

Debt-to-income (DTI) ratios provide another point of divergence. FHA guidelines offer significant breathing room, often permitting a DTI up to 50% or higher if compensating factors exist. Conventional lenders usually cap this at 43% to 45%. When it’s time for the appraisal, the U.S. Department of Housing and Urban Development mandates strict safety and soundness inspections for FHA properties. Conventional appraisals focus primarily on market value, offering more flexibility for “fixer-upper” sanctuaries that might need cosmetic repairs before move-in.

- Credit Score: 580 (FHA) vs. 620+ (Conventional)

- Down Payment: 3.5% (FHA) vs. 3% (Conventional First-Time Buyer)

- DTI Cap: 50%+ (FHA) vs. 45% (Conventional)

- Appraisal: Health and safety focus (FHA) vs. Value and condition focus (Conventional)

2026 Santa Clara County Loan Limits

Gilroy sits within a high-cost region, which elevates the borrowing ceiling for local residents. For 2026, the FHA loan limit for single-family homes in Santa Clara County is expected to hold at the floor of $1,149,825, matching the high-balance conforming limit. This alignment allows buyers to secure substantial financing without immediately jumping into complex private products. In Santa Clara County, any mortgage exceeding the 2026 high-balance limit of $1,149,825 for a single-family home is classified as a Jumbo loan.

The Mortgage Insurance Divide

The cost of insurance is where these two paths truly separate. FHA loans require a Mortgage Insurance Premium (MIP) that includes both an upfront fee of 1.75% and an annual premium paid monthly. If you put down less than 10%, this MIP remains for the life of the loan, regardless of how much equity you build. Conventional loans utilize Private Mortgage Insurance (PMI), which doesn’t require an upfront payment and is based entirely on your credit score. Most importantly, you can cancel PMI on a conventional loan once your principal balance reaches 80% of the original value. Understanding these nuances is part of the collaborative partnership we offer to ensure your home remains a stable financial asset for years to come.

The Gilroy Factor: Which Loan Wins the Bidding War?

Gilroy’s real estate market demands a strategic approach. In neighborhoods like Eagle Ridge, where the median sales price often exceeded $1.4 million in late 2023, the choice between an fha loan vs conventional gilroy buyers face can dictate whether an offer is even considered. Sellers in mature areas like Las Animas often prioritize certainty over the highest price. They sometimes view FHA offers as “risky” due to perceived red tape. This perception is a myth we actively debunk. We present your FHA offer alongside a comprehensive pre-approval letter and a track record of 100% on-time closings. This shifts the narrative from risk to reliability. We don’t just submit paperwork; we build a case for your financial integrity.

Navigating FHA Appraisal Requirements

FHA appraisals focus on safety and habitability. Common Gilroy property issues, such as peeling lead-based paint in homes built before 1978 or missing handrails on steep driveways, can trigger repair demands. According to the Consumer Financial Protection Bureau, these loans are designed to protect the buyer’s investment, yet sellers fear the extra cost. We handle these negotiations by identifying potential flags during the initial walkthrough. If an appraiser identifies a $500 safety fix, we coordinate the solution immediately rather than letting the deal stall. Modern real estate moves fast; an FHA loan isn’t a deal breaker when managed with precision.

The Conventional Edge in Multiple-Offer Scenarios

Conventional loans often hold the upper hand when competing against Silicon Valley’s cash-heavy buyers. A conventional offer with a 20% down payment signals immense financial strength to a Gilroy seller. It allows for shorter appraisal contingencies, sometimes as brief as 10 days, which appeals to sellers wanting a seamless exit. Integrity Estates Realty positions your offer for maximum reliability by highlighting your debt-to-income ratio and solid assets. We bridge the gap between financial logic and the seller’s desire for a legacy-worthy buyer. While cash is fast, a well-structured conventional loan is just as certain. Our goal is to curate a strategy that reflects your lifestyle goals while respecting the seller’s need for a smooth transition.

- Speed: Conventional loans can often close 5 to 7 days faster than FHA counterparts in Santa Clara County.

- Flexibility: Conventional guidelines allow for easier financing on “fixer-upper” properties that might fail FHA inspections.

- Perception: A 10% or 20% down payment on a conventional loan suggests a buyer with deep reserves, which provides peace of mind to the listing agent.

Financial Strategy: Long-Term Costs and Refinancing

Analyzing the true cost of an fha loan vs conventional gilroy requires looking far beyond the initial monthly payment. While FHA loans often carry lower interest rates, the 1.75% upfront mortgage insurance premium and the recurring annual charges can add approximately $48,000 to the total cost of a $900,000 home over a 30-year period. Conventional loans avoid these permanent fees once you reach 20% equity, making them a more efficient vehicle for long-term wealth. By 2026, economic forecasts suggest the spread between FHA and conventional rates will hover around 0.45%. This gap makes FHA an attractive entry point for those with limited capital, but the math favors a conventional transition as soon as your financial profile strengthens. Eligible service members should also consider how the va home loan benefits california veterans receive — including no down payment and no private mortgage insurance — can make this long-term cost comparison even more favorable.

Closing costs in California add another layer of complexity. In a typical Gilroy transaction, buyers should budget for 2% to 3% of the sales price to cover escrow fees, appraisals, and title insurance. Sellers in Santa Clara County generally pay the documentary transfer tax of $1.10 per $1,000 of the sale price. We ensure our clients understand these line items clearly so there are no surprises at the finish line.

The Refinance Roadmap

Refinancing is a strategic exit from higher-cost insurance. Many Gilroy residents use an fha home loans gilroy program to secure a home in a competitive market, then pivot to a conventional loan once they’ve built sufficient equity. Gilroy property values saw a 6.2% increase between 2023 and 2024, a trend that helps homeowners reach the 20% equity threshold faster than the national average. A refinance becomes a logical choice when your monthly savings from dropping the mortgage insurance recoup the new loan’s closing costs within 22 months.

Tax Implications and Benefits

California tax laws provide specific advantages for homeowners managing high-value assets. You can generally deduct interest on the first $750,000 of mortgage debt on your federal returns, providing a significant shield for your income. Deciding on an fha loan vs conventional gilroy path is a decision about your financial legacy. We view every transaction as a collaborative partnership, focusing on lifestyle curation rather than just a property swap. Your home should be a sanctuary that grows your net worth while providing peace of mind. Our team acts as a steadfast guide to ensure your loan structure aligns with your five-year and ten-year wealth goals.

Your Gilroy Partnership: Integrity Estates Realty & Mortgage

Deciding between an fha loan vs conventional gilroy requires more than a standard calculator; it demands a partner who understands the local soil. At Integrity Estates Realty, we offer a rare, unified approach by housing both real estate and mortgage services under one roof. Maria Elena “Nena” Arriaga has provided ethical guidance across California for 22 years, helping families navigate the complexities of home ownership since 2002. This integration eliminates the friction often found between separate realtors and lenders, ensuring your lifestyle goals dictate your loan choice rather than the other way around.

Our team doesn’t just process applications. We conduct personalized market analyses that reflect the current 95020 inventory. We match the loan to the sanctuary you desire, ensuring that whether you choose a low-down-payment FHA option or a competitive conventional product, the transition from pre-approved to key-in-hand is seamless. We’ve managed over 1,000 successful closings by prioritizing the human story behind every front door.

Our Commitment to Transparency

Integrity is our thematic promise. While 68% of home buyers report feeling overwhelmed by hidden fees, we operate with absolute clarity. We intentionally avoid the bait-and-switch tactics used by big-box lenders who prioritize volume over people. By focusing on ethical real estate, we help you build a legacy for your family. We treat your mortgage as the financial foundation of your home, stripping away the stress to provide a calm, methodical path toward property ownership.

Next Steps for Gilroy Buyers

Your journey toward a new home begins with a clear financial picture. We invite you to start your pre-qualification process today to see how your numbers align with the Gilroy market. Our experts are available for private consultations at our Arroyo Circle office, where we can compare the specific benefits of an fha loan vs conventional gilroy based on your current credit profile and savings.

- Review your 2024 debt-to-income ratios with a professional.

- Analyze local property taxes and insurance premiums for the Santa Clara County area.

- Create a custom roadmap from initial offer to final signatures.

Don’t leave your future to chance or automated algorithms. Speak with a Gilroy Mortgage Expert at Integrity Estates Realty to secure a partner who is as invested in your future as you are.

Secure Your Gilroy Legacy in 2026

Choosing between an fha loan vs conventional gilroy in 2026 requires more than just a credit check; it demands a strategy that accounts for evolving loan limits and the competitive landscape of Santa Clara County. Success in this market hinges on understanding how a 3.5% down payment via FHA compares to the lower insurance costs of a conventional mortgage over a 30-year term. Whether you’re aiming for a suburban sanctuary or a long-term investment, the right choice protects your legacy and ensures a seamless transition into homeownership.

Maria Elena “Nena” Arriaga and the team at Integrity Estates Realty & Mortgage bring over 20 years of experience to your side. As an independently owned firm serving Santa Clara and Monterey Counties, we offer a rare dual expertise in both real estate and mortgage origination. This unified approach eliminates the friction between finding a home and securing the funds. We prioritize your peace of mind by acting as an ethical anchor throughout your journey, ensuring every detail aligns with your financial goals.

Start Your Gilroy Home Search with a Trusted Mortgage Partner

Your dream home in Gilroy is within reach when you have a partner who values your story as much as the transaction.

Frequently Asked Questions

Is an FHA loan better than a conventional loan for a first-time buyer in Gilroy?

The choice depends on your current credit profile and available capital. An FHA loan is often the preferred path for those with a credit score near 580, as it requires only a 3.5% down payment. When comparing an fha loan vs conventional gilroy residents often find that conventional loans offer more long-term savings if they have a 620 score or higher. We view this decision as the foundation of your financial legacy, so choosing the right vehicle is essential for your peace of mind.

Can I buy a house in Gilroy with 3% down on a conventional loan?

Yes, qualified buyers can access 3% down payment programs like HomeReady or Home Possible. For a median-priced Gilroy home of $950,000, this means an initial investment of $28,500. This path allows you to secure a sanctuary without the permanent mortgage insurance requirements tied to government-backed loans. It’s a sophisticated way to enter the market while keeping more of your liquidity for home improvements or future investments.

What are the 2026 FHA loan limits for Santa Clara County?

While HUD announces exact figures annually, the 2024 limit for Santa Clara County stands at $1,149,825 for single-family homes. Based on the 5.2% average annual appreciation seen in the local market, projections suggest the 2026 limit could reach approximately $1,270,000. These adjustments ensure that your journey toward homeownership remains viable even as property values in our community continue to climb. We track these metrics closely to provide you with the most reliable market analysis.

Does FHA mortgage insurance ever go away?

FHA mortgage insurance remains for the entire life of the loan if your down payment is less than 10%. If you contribute 10% or more at closing, the insurance premium naturally expires after 11 years. In the fha loan vs conventional gilroy debate, this is a pivotal factor because conventional private mortgage insurance automatically cancels once you reach 22% equity. Understanding these nuances is part of our commitment to transparency and ethical guidance.

Why do sellers in Gilroy sometimes prefer conventional loans over FHA?

Sellers often perceive conventional offers as more stable because they typically involve buyers with higher credit scores and fewer property condition requirements. FHA appraisals follow strict HUD safety guidelines, which means a home with minor issues like peeling paint or a missing handrail must be repaired before the sale closes. In a competitive market where 45% of homes receive multiple offers, a conventional loan can offer a more seamless escrow process. We act as your steadfast guide to ensure your offer stands out regardless of your financing choice.

What is the minimum credit score for a conventional loan in California?

Most lenders require a minimum FICO score of 620 to qualify for a conventional mortgage. However, securing a score of 740 or higher typically unlocks the most favorable interest rates and lower insurance premiums. Maintaining high credit standards ensures your mortgage remains a tool for wealth creation rather than a financial burden. We believe in a collaborative partnership, helping you understand how your credit score impacts the story of your home.

Can I use an FHA loan for a condo in Gilroy?

You can use an FHA loan for a condo, but the entire complex must be on the HUD-approved list. Currently, only about 7% of California condominium projects maintain this certification. If your desired sanctuary isn’t on the list, we can pursue a single-unit approval process to facilitate the transaction. This methodical approach ensures no detail is overlooked in your pursuit of the perfect Gilroy lifestyle.

How much are closing costs for a home in Gilroy?

Buyers in Santa Clara County should expect closing costs to range between 2% and 5% of the final purchase price. On an $800,000 property, this totals between $16,000 and $40,000 for items like title insurance, escrow fees, and prepaid taxes. We prioritize your peace of mind by providing a detailed breakdown of these costs early in the process. There are no surprises here; just a clear, professional path to your new front door.