Jumbo Loan Rates in San Francisco: Your 2026 Comprehensive Buying Guide

In the high-stakes landscape of San Francisco real estate, waiting for the perfect market moment often costs more in lost equity than a fraction of a percentage point ever could. Your home is a sanctuary and a legacy; however, in a city where the conforming loan limit for a one-unit property has reached $1,249,125 as of May 2026, the financial strategy behind that sanctuary must be flawless. You likely feel the pressure of market volatility and the complexity of non-conforming loan requirements. Securing competitive jumbo loan rates san francisco offers requires a partner who understands that your tech-equity compensation is a strength, not a hurdle.

We believe the mortgage process should be a collaborative partnership rooted in transparency and peace of mind. This guide provides a clear look at the current market trends, including the national 30-year fixed jumbo rate average of 6.53% as of May 3, 2026. You’ll learn how to navigate strict qualification standards, such as the typical 43% debt-to-income ratio, while positioning yourself for a low-interest rate. We’ll walk through the specific steps to minimize your closing costs and maximize your future equity in the city we call home.

Key Takeaways

- Understand the current landscape of jumbo loan rates san francisco and how recent market shifts influence your luxury property purchasing power.

- Identify the 2026 FHFA conforming loan limits to determine exactly when your financing moves into high-balance or true jumbo territory.

- Evaluate the strategic benefits of Adjustable-Rate Mortgages (ARMs) versus fixed-rate options based on the unique homeownership cycles of the Bay Area.

- Prepare your financial profile by mastering the specific credit score and debt-to-income benchmarks required by elite wholesale lenders.

- Discover how a collaborative partnership with a local market expert can streamline your mortgage process and protect your long-term equity.

Current Jumbo Loan Rates in San Francisco: 2026 Market Outlook

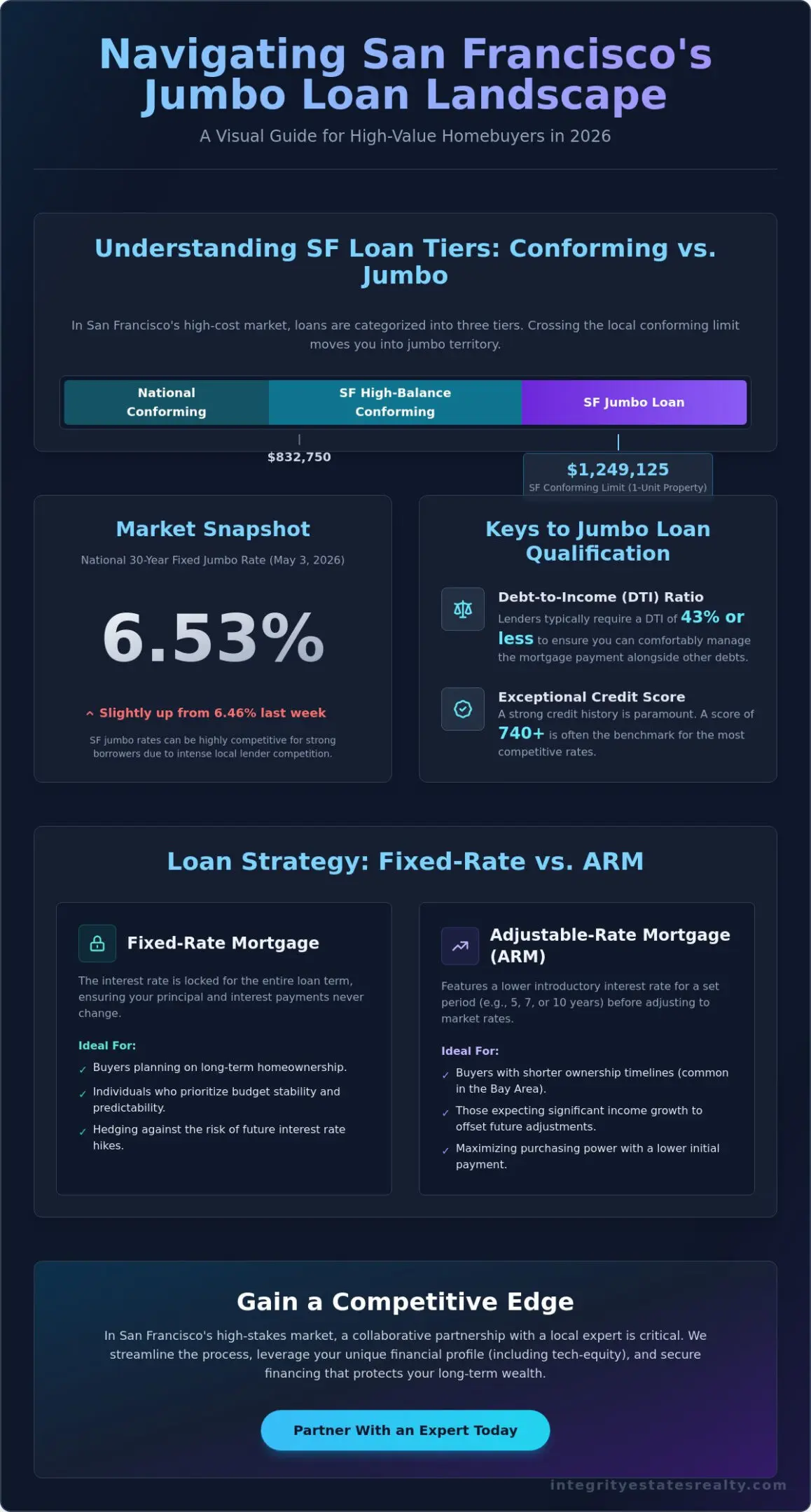

San Francisco’s real estate market operates on a scale that defies national averages. As of May 3, 2026, the national average for a 30-year fixed jumbo mortgage sits at 6.53%, up slightly from 6.46% the week prior. In our local market, these figures are more than just numbers; they represent the entry point for homeowners seeking a sanctuary in one of the world’s most competitive landscapes. A jumbo loan is a mortgage that exceeds the FHFA conforming loan limits for high-cost counties. For 2026, that limit for a one-unit property in San Francisco is $1,249,125. If your financing needs surpass this threshold, you’re officially in the jumbo tier. Understanding What is a Jumbo Loan? is the first step in recognizing why these products require a more sophisticated approach to underwriting. Because these loans aren’t guaranteed by Fannie Mae or Freddie Mac, lenders carry the full risk, which directly impacts the jumbo loan rates san francisco buyers see on their term sheets.

The 2026 Economic Landscape for Bay Area Buyers

Inflationary trends and Federal Reserve policies through the first half of 2026 have introduced a layer of complexity to luxury financing. Local tech sector performance remains a vital indicator of mortgage liquidity in the Bay Area. When stock-based compensation models are robust, lenders often show a greater appetite for jumbo products, occasionally offering more aggressive pricing to secure high-net-worth relationships. However, volatility is a constant companion in this coastal market. It’s essential to monitor daily shifts and move decisively when a favorable window opens. Locking in a rate isn’t just about the monthly payment; it’s about protecting your long-term equity and ensuring your home remains a stable asset for your family’s legacy.

Why San Francisco Rates Carry a “High-Cost” Nuance

Lending in the city involves a unique distinction between “high-balance” conforming loans and true jumbo financing. High-balance loans cover the gap between the national conforming limit of $832,750 and our local limit of $1,249,125. Once you move past that $1.25 million mark, the rules of the game change. Local lenders compete fiercely for SF clients, which can sometimes result in jumbo rates that are surprisingly competitive compared to standard conforming products. This dynamic is specific to high-density wealth centers. For a broader perspective on how geography influences pricing, you can compare these figures to Gilroy real estate market trends, where lower loan balances and different inventory levels create a separate financial narrative. We treat every transaction as a partnership, bringing a sense of integrity to the process so you can focus on the story behind your new front door.

Conforming vs. Jumbo: Navigating High-Balance Limits in 2026

The distinction between a conforming loan and a jumbo mortgage isn’t just a technicality; it’s a financial threshold that dictates the trajectory of your homeownership journey. In San Francisco and Santa Clara counties, the Federal Housing Finance Agency (FHFA) has set the 2026 conforming loan limit for a one-unit property at $1,249,125. This figure represents a significant increase from years past, yet it often falls short of the prices found in our city’s most coveted neighborhoods. When your loan amount exceeds this “high-balance” ceiling, you enter the territory of non-conforming loans. At this level, jumbo loan rates san francisco lenders offer are no longer governed by federal guarantees, leading to a shift in how risk is priced and how your financial profile is scrutinized.

Choosing between these two categories requires a careful analysis of the interest rate spread. Traditionally, jumbo rates carried a premium, but in the current 2026 market, that gap has narrowed. High-balance conforming loans, which cover the space between the national limit of $832,750 and the local high-cost limit of $1,249,125, often serve as a bridge. However, once you cross into true jumbo territory, you’ll find that lenders prioritize high-net-worth relationships, sometimes offering competitive pricing that rivals conforming products for borrowers with exceptional credit. Understanding the nuances of Qualifying for a Jumbo Mortgage is essential for anyone looking to secure a property above the $1.5 million mark.

The Financial Impact of Crossing the Jumbo Threshold

Crossing into jumbo territory changes your liquidity requirements immediately. While some high-balance conforming programs allow for lower down payments, true jumbo loans in San Francisco typically require at least 20% down. Lenders also look for deep cash reserves, often demanding six to 12 months of mortgage payments held in liquid accounts. These stricter standards ensure the stability of the loan, but they also mean you must be prepared to tie up more capital upfront. This shift can impact your monthly cash flow and your broader investment strategy, making it vital to weigh the benefits of a larger loan against the security of higher liquid reserves.

Strategic Down Payments in a High-Price Market

Many savvy buyers in the Bay Area choose to “buy down” their loan amount to stay within the high-balance conforming limit. By increasing your down payment to keep the borrowed amount at exactly $1,249,125, you might access more flexible underwriting and lower reserve requirements. This strategy requires a balance between your tax objectives and your desire for long-term equity. Consulting with experienced mortgage brokers in Santa Clara County can help you determine if the interest deduction benefits of a larger jumbo loan outweigh the simpler requirements of a conforming product. We invite you to connect with our team to explore which path aligns best with your vision of a home as both a sanctuary and a strategic asset.

Fixed-Rate vs. ARM: Choosing the Right Strategy for SF Real Estate

Selecting a mortgage structure is as personal as selecting the neighborhood itself. In a city where property values often exceed the $1,249,125 limit defined by the Consumer Financial Protection Bureau, the spread between fixed and adjustable options becomes a critical calculation. For many, the jumbo loan rates san francisco lenders provide for 7/1 or 10/1 Adjustable-Rate Mortgages (ARMs) offer an attractive entry point. These products are particularly popular among the city’s mobile professional workforce. If you expect to relocate or upgrade your residence within a decade, an ARM allows you to maximize your monthly cash flow during the initial fixed period. It’s a sophisticated strategy that treats your mortgage as a flexible financial tool rather than a static debt.

While the allure of lower initial payments is strong, the 30-year fixed jumbo remains the anchor for those seeking a permanent sanctuary. There’s an undeniable peace of mind that comes from knowing your principal and interest payment will never change, regardless of how the global economy shifts over the next three decades. We believe in providing the transparency you need to choose between short-term flexibility and long-term security. Every home tells a story, and your financing should support the lifestyle you intend to curate within those walls. Whether you’re eyeing a contemporary loft in SoMa or a legacy estate in Pacific Heights, the right rate structure protects your equity and your peace of mind.

When a 7/1 or 10/1 ARM Makes Financial Sense

As of May 3, 2026, local institutions like SF Fire Credit Union have offered 10/1 ARMs at 5.750%, providing a significant discount compared to the 6.53% national average for 30-year fixed jumbos. This strategy works well for borrowers who plan to sell or refinance before the first rate adjustment occurs. You’ll need to calculate the break-even point by comparing the total interest saved during the fixed term against the potential costs of a future transaction. It’s a methodical approach that prioritizes keeping your capital liquid for other investments or lifestyle needs during those early years of homeownership.

The Case for the 30-Year Fixed Jumbo

The current 2026 market shows a spread between fixed and adjustable jumbo rates of approximately 0.75% to 1.00%. For families who view their home as a forever sanctuary, paying this premium is often worth the insurance against future volatility. You won’t have to worry about market resets or the stress of a mandatory refinance window. If rates do drop significantly in the future, you always have the option to pivot. Our refinance mortgage Gilroy guide explores these equity-saving strategies in detail, ensuring you’re positioned to capture lower rates if the economic cycle shifts in your favor.

Qualifying for a Jumbo Mortgage: Requirements & Credit Scores

Securing a high-value mortgage in the Bay Area requires more than just a substantial income; it demands a financial profile that radiates stability and precision. While national guidelines often suggest a credit score of 700 is sufficient, the most competitive jumbo loan rates san francisco lenders offer are typically reserved for those with a FICO score of 740 or higher. In many cases, elite wholesale lenders in the city look for 760+ to unlock the absolute floor of available pricing. This higher bar reflects the unique nature of our local market, where loan amounts frequently double or triple the national average. We approach this process with a commitment to integrity, ensuring you understand every benchmark before your application reaches the underwriter’s desk.

Your debt-to-income (DTI) ratio is the second pillar of jumbo qualification. Most luxury lenders prefer a DTI of 43% or lower, though some boutique programs may offer flexibility for borrowers with significant liquid assets. For the tech-driven workforce of San Francisco, documenting income involves more than just a W-2. We specialize in helping clients navigate the complexities of Restricted Stock Units (RSUs), stock options, and performance bonuses. Underwriters typically require a two-year history of these earnings to count them toward your qualifying income. This meticulous approach ensures that your financing is as reliable as the sanctuary you’re looking to purchase. If you’re ready to see how your portfolio aligns with current standards, you can schedule a private consultation with our team today.

Asset Reserves and Liquidity Requirements

Lenders want to know you can weather a financial storm without risking your home. For a jumbo loan, you’ll generally need to demonstrate six to 12 months of mortgage payments held in reserve. These reserves provide a safety net for both you and the lender. When gathering your documentation, remember that various asset types carry different weights:

- Cash and Savings: Counted at 100% of their value.

- Brokerage Accounts: Stocks and bonds are typically valued at 70% to 80% to account for market volatility.

- Retirement Accounts: 401(k) and IRA balances may be considered, often at 60% to 70% of their vested value.

Appraisal Nuances for High-Value Properties

Valuing a Victorian in Pacific Heights or a modern masterpiece in Sea Cliff requires a specialized eye. Because jumbo loans represent a higher concentration of risk, lenders often require two independent appraisals for properties exceeding a certain price point, usually $2 million. These reports must account for unique architectural features and historical significance that standard algorithms might miss. In a competitive bidding environment, appraisal gaps can occur. We work closely with you to develop a strategy for these scenarios, ensuring that a conservative valuation doesn’t stand in the way of your dream home.

Beyond the Rate: The Integrity Estates Partnership

Securing a competitive interest rate is a significant milestone, but it’s only one chapter in the story of your home purchase. In a landscape where jumbo loan rates san francisco lenders offer can fluctuate weekly, having a partner who views your mortgage as a component of a larger legacy is essential. We don’t just process loans; we provide a sophisticated, integrated brokerage experience that bridges the gap between financial logic and your lifestyle aspirations. Our team brings deep local expertise to every transaction, whether you’re searching for a modern high-rise in San Francisco, a tech-adjacent estate in San Jose, or a quiet retreat in Salinas. This regional knowledge ensures that your financing strategy is perfectly aligned with the specific nuances of the neighborhood you choose to call home.

We believe that true value lies in the synergy between real estate representation and mortgage expertise. By housing these services under one roof, we eliminate the friction often found in high-value transactions. This collaborative model allows us to protect your interests with a level of precision that traditional lenders simply cannot match. If you’re exploring the broader Bay Area market, viewing homes for sale in Gilroy serves as an excellent starting point to understand how luxury financing and property value intersect in today’s 2026 market. We treat every client relationship as a long-term partnership, prioritizing transparency and ethical conduct over quick sales.

A Collaborative Path to Your California Sanctuary

Working with Maria Elena “Nena” Arriaga means experiencing a concierge level of service that transforms a complex process into a seamless journey. We act as your steadfast guide, coordinating every detail between lenders, escrow officers, and sellers to ensure a calm and purposeful closing. This hands-on approach is designed to alleviate the stress of the SF luxury market, allowing you to focus on the curation of your new sanctuary. Integrity is more than our name; it’s a recurring thematic promise that dictates how we negotiate on your behalf. We advocate for your equity with the same dedication we would our own, ensuring that every financial decision strengthens your long-term position.

Next Steps: Securing Your 2026 Jumbo Pre-Approval

In the fast-paced San Francisco market of May 2026, a pre-approval is your most powerful tool. It signals to sellers that you’re a serious, qualified buyer who has already mastered the complexities of jumbo loan rates san francisco requirements. Our team is ready to provide a personalized mortgage consultation that examines your specific income structure, including RSUs and bonuses, to establish a clear path forward. This proactive step gives you a decisive speed advantage when the right property appears. We invite you to begin this journey with us, building a lasting legacy through smart, intentional real estate investment. Your dream home is more than an asset; it’s the backdrop for your future, and we’re here to ensure that foundation is secure.

Your Path to a San Francisco Sanctuary

Navigating the complexity of the 2026 luxury market requires more than just a financial transaction; it demands a strategic vision for your future. We’ve detailed how the high-cost conforming limit of $1,249,125 shapes the financing landscape and why current jumbo loan rates san francisco lenders provide are best captured through meticulous preparation. From mastering credit score benchmarks to choosing between fixed-rate stability and adjustable flexibility, your journey to homeownership should be defined by clarity and confidence.

At Integrity Estates Realty, we offer over two decades of California real estate and mortgage expertise to guide you through every nuance of the process. Our integrated brokerage and lending model ensures a seamless closing experience, allowing you to focus on the life you’re building. As an independently owned and operated firm, we’re dedicated to ethical partnerships that prioritize your peace of mind above all else. Your dream home is a legacy in the making, and we’re honored to be your steadfast guide. Secure Your San Francisco Jumbo Pre-Approval with Integrity Estates Realty and take the first step toward your new front door today.

Frequently Asked Questions

What is the current jumbo loan limit for San Francisco in 2026?

For a one-unit property in 2026, the conforming loan limit in San Francisco is $1,249,125. Any mortgage amount that exceeds this threshold is classified as a jumbo loan. For those looking at multi-unit properties, the limits increase significantly; a two-unit property has a limit of $1,599,375, while four-unit properties reach up to $2,402,625 before entering jumbo territory. Understanding these specific boundaries is the first step in crafting a successful financing strategy for your Bay Area sanctuary.

Are jumbo loan rates higher or lower than conforming rates in the Bay Area?

Jumbo loan rates in San Francisco often fluctuate near or slightly below conforming rates because local lenders compete fiercely for high-net-worth clients. As of May 3, 2026, the national average 30-year fixed jumbo rate is 6.53%. In our local market, sophisticated borrowers often find that non-conforming products offer surprisingly aggressive pricing. This unique dynamic exists because lenders view these high-value loans as the foundation for long-term, multi-service financial partnerships with established professionals.

How much down payment is required for a jumbo loan in San Francisco?

A down payment of 10% to 20% is typically required for most jumbo loan programs in the 2026 San Francisco market. While 20% remains the standard for securing the most favorable terms and avoiding additional risk premiums, many competitive lenders now offer paths with just 10% or 15% down for highly qualified buyers. These lower down payment options allow you to preserve your liquid capital for other investments while still securing a high-value property in a premier neighborhood.

Can I get a jumbo loan with a 10% down payment?

Yes, you can secure a jumbo loan with a 10% down payment if you meet specific credit and reserve benchmarks. Lenders offering these terms usually require a FICO score of 740 or higher and significant cash reserves, often totaling 12 months of mortgage payments. This approach is a popular choice for professionals who want to maximize their leverage while maintaining a robust investment portfolio. It’s a strategic way to transition into a new home without tying up excessive amounts of upfront capital.

How do lenders view RSU income for jumbo loan qualification in SF?

Lenders typically accept Restricted Stock Units (RSUs) as qualifying income if you can demonstrate a consistent two-year history of receipt and a clear vesting schedule for the future. Because the San Francisco economy is rooted in the tech sector, local luxury lenders have developed sophisticated models to calculate the value of stock-based compensation. They’ll analyze your vesting history and current stock performance to determine a stable income average, ensuring your total compensation package is fully recognized during the underwriting process.

What credit score do I need for the best jumbo mortgage rates?

You generally need a credit score of 740 or higher to access the most competitive jumbo loan rates san francisco lenders currently offer. While some programs may accept a score as low as 680 or 700 with a larger down payment, the lowest interest rates are reserved for those in the top tier. Maintaining a high score is essential for minimizing your long-term borrowing costs. We prioritize transparency in this process, helping you understand exactly how your credit profile impacts your final term sheet.

Is it better to get a fixed-rate or an ARM for a jumbo loan in 2026?

The choice between a fixed-rate and an Adjustable-Rate Mortgage (ARM) depends entirely on your expected duration in the home. In May 2026, 10/1 ARMs have been offered at rates like 5.750%, providing a lower initial payment for those who plan to sell or refinance within a decade. If you’re establishing a permanent family sanctuary and want to avoid any future market volatility, the 30-year fixed mortgage remains the gold standard for long-term peace of mind and financial predictability.

Do jumbo loans require private mortgage insurance (PMI)?

Jumbo loans typically do not require traditional private mortgage insurance even when your down payment is less than 20%. Instead of a separate monthly PMI fee, lenders often account for the increased risk by adjusting the interest rate slightly or using lender-paid mortgage insurance. This structure keeps your monthly payment simple and predictable. It’s part of a seamless mortgage experience designed to cater to the needs of high-net-worth individuals who value efficiency and financial clarity.